At SIFMA, we believe that public policy and financial regulation should support these key tenets:

- Ensure high standards of market integrity and investor protection

- Encourage pools of capital through private and public pensions

- Promote financial literacy and a strong retail investor culture

- Calibrate supervision and regulation with robust capital formation and growth

What follows are our viewpoints on several key issues facing the capital markets and financial industry today. To learn more about these and other topics, visit www.sifma.org/issues.

The Post-COVID Agenda

When the virus emerged in the first quarter of 2020, the financial sector quickly implemented business continuity plans and entered a prolonged period of extreme market volatility. At the peak, the industry was operating with approximately 90% of personnel working remote. Over the following several months, the industry and the markets adjusted to the impacts of the pandemic, making a range of changes to operating models, use of technologies and market activities.Throughout the crisis, financial industry regulators provided the industry with emergency relief measures to ensure that the markets could continue to function effectively with most personnel working remote, travel restrictions, and increased volatility in the marketplace. While the level of remote working remains high, SIFMA believes regulators and the industry should develop rules and protocols for a post-COVID environment.

With vaccines in sight, now is the time to consider the “new normal.”

Modernizing the Delivery of Financial Communications

The COVID-19 pandemic has only magnified the shift to an internet-based world. The overall move to electronic delivery is not limited to investment-related documents. From health care explanations of benefits to income tax reporting, the trend toward electronic delivery is undeniable and for good reason. Delivering materials electronically provides individuals with real-time, up-to-date access to information, along with other online tools that can assist with financial management.

At a time when many in the country have moved their personal, professional, and educational lives online, the production and mailing of communications in paper form raises logistical and health concerns, and digital tools are increasingly being leveraged to protect public health and ensure continued access to information. SIFMA has long supported the electronic delivery of retirement and mutual fund disclosures and other investment-related communications. Investors from all demographics increasingly prefer to access information electronically and believe that doing so makes it easier to act on that information.

Electronic delivery can also make information more accessible in other languages and in specialized formats for those with disabilities. For financial services, the interactive nature of electronic access via links and embedded information can make investor action and engagement easier and more likely to occur. In fact, studies have found that 401(k) participants who interact with their plans’ websites tend to have higher contribution rates.

Electronic delivery is also more environmentally friendly than paper and significantly reduces production and shipping costs. It is important to note that paper communications would remain an option for those who prefer paper or do not have access to reliable internet service.

e-Delivery Discussion Paper

www.sifma.org/e-delivery

In this discussion paper, the Securities and Exchange Commission (SEC) is urged to update its rules and related guidance to allow the implementation of a digital approach establishing electronic delivery as the primary means for delivering investor communications. Any investor wishing to receive paper communications can continue to do so.

Dematerialization

Dematerialization refers to fully transitioning securities processing from physical certificates to electronic records.

The Depository Trust and Clearing Corporation (DTCC) issued a paper to build consensus among stakeholders on critical next steps to reduce, and ultimately eliminate, certificated U.S. securities. Dematerialization would reduce the risks and costs associated with manual processing and human touchpoints, as well as increase efficiency and resiliency across the industry at a time when automation is more important than ever. Less than 1% of assets serviced by DTCC, through the firm’s subsidiary The Depository Trust Company (DTC), are still in physical form, but they represent $780 billion dollars in value.

SIFMA appreciates the work of the DTCC as our industry works to achieve full dematerialization in the U.S. financial markets. SIFMA is actively engaged with DTCC and other industry partners as we work to eliminate both the issuance and handling of physical securities, which will result in a more cost-effective, efficient, transparent, secure, competitive, and resilient marketplace. The COVID-19 crisis is a real-world example highlighting the need for change, as the processing of physical securities was disrupted and delayed, while handling certificates issued in paperless form were seamless. SIFMA will continue our deep engagement with the industry on this initiative.

Unique Considerations for Asset Managers

There is a need for regulatory modernization specific to asset managers. These issues include expanded and permanent relief for interfund lending and cross-trading, which would provide firms with additional tools to address market disruptions in the future. COVID-19 has also brought to light operational challenges associated with utilizing swing pricing, which is technically permitted under current regulations but not actually available without addressing certain marketplace practices. SIFMA and SIFMA’s Asset Management Group (AMG) directly work with state and federal regulators regarding regulatory relief needs due to the health crisis. SIFMA advocates for the SEC to amend the relevant investor communications rules to allow for electronic delivery to become the default for all investor communications. SIFMA also believes that the SEC should permanently permit board meetings to be held virtually.

Future of Work

As firms develop reemergence plans, now is the time to think critically about how the “new normal” will drive the future of work. Lessons learned in the past several months should guide firms’ assessment of which operational

practices should remain in place going forward, and what metrics best demonstrate the ability to respond to a crisis and to operate efficiently, and whether certain business continuity initiatives should be accelerated or disregarded should be also part of the analysis.

Going forward, the industry should continue to collaborate with regulators to put in place critical regulatory relief during the pandemic, including forms of necessary relief that would promote working remotely, trading virtually, and extending the filing deadlines for statutory reports. This also means institutions should continue to pay close attention to any forthcoming regulatory guidance to stay current on new requirements.

As the industry does return to normal working arrangements, firms should work with regulators and infrastructure providers to identify opportunities to make permanent the more efficient operating models adopted during the pandemic.

There are many factors involved when making the decision to have staff return to the office, including safety, legal and liability concerns, employee sentiment and privacy, availability of rapid health screening and testing, human resources policies, local government directives and health care advisories as well as the practical and logistical issues around maintaining social distancing within the office. SIFMA has published Considerations for Return to Office, which each individual firm should use to make individual decisions regarding their strategy and tactics for the new operating environment. As this situation evolves and as firms start to execute their plans, other considerations will undoubtedly arise as firms better understand how returning staff to the office will work in practice and evaluate the resulting lessons learned.

Improving American Infrastructure Through Municipal Finance

www.sifma.org/muniSIFMA and its member firms support the preservation of the tax exemption for municipal bonds as well as four main initiatives that help promote increased bond financing and fund important infrastructure-related projects while also saving taxpayer dollars:

- Secure the passage of legislation permitting issuers to advance refund tax-exempt municipal debt;

- Authorize a new direct payment bond program on a permanent basis;

- Expand the volume cap and uses for Private Activity Bonds (PABs); and

- Increase the annual limit on the amount of tax-exempt obligations that may be issued to qualify for the small issuer exception to the tax-exempt interest expense allocation rules.

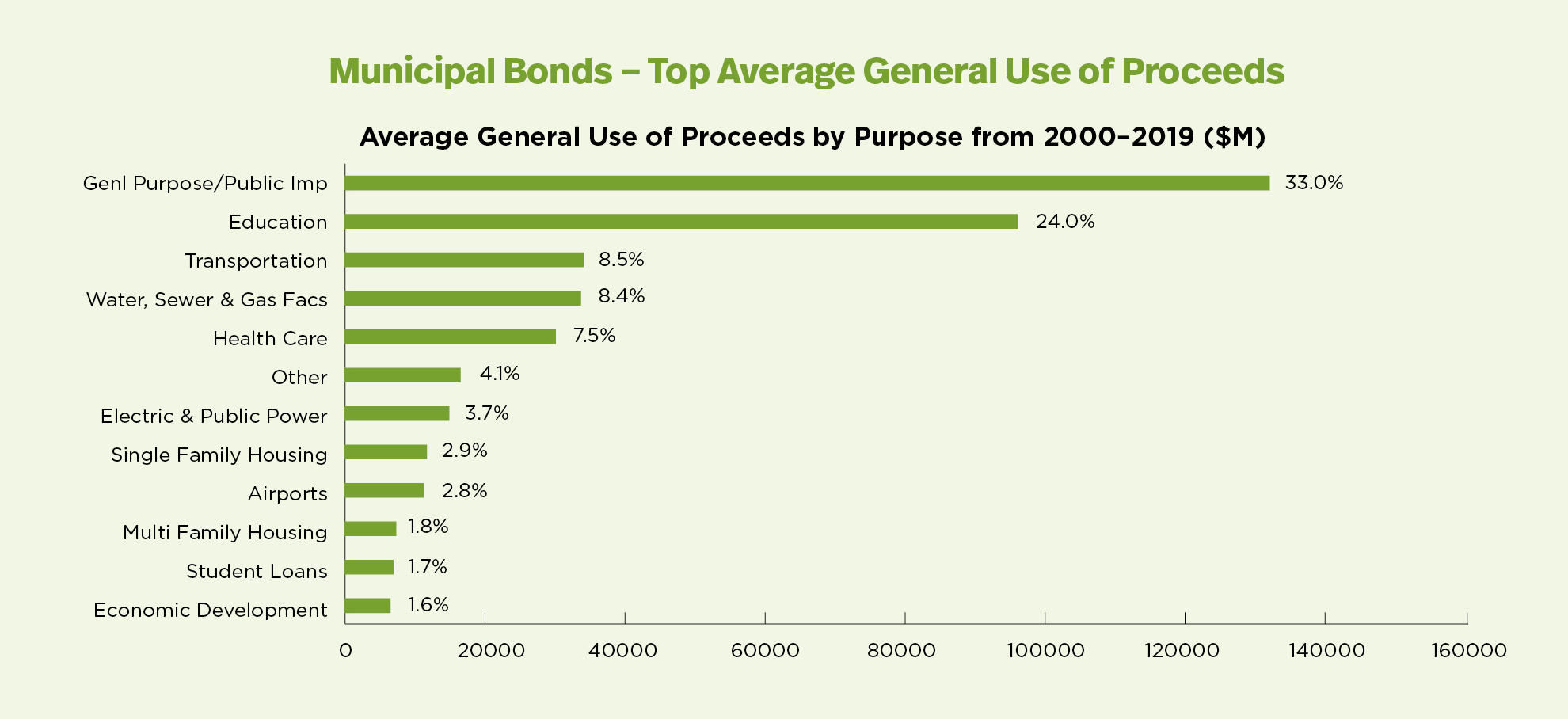

The American Society of Civil Engineers (ASCE) estimates that the U.S. needs to invest $4.6 trillion in infrastructure by 2025 to replace failing facilities, maintain our global competitiveness, and supply the capacity needed by a growing economy and population. They also estimate that the failure to close this infrastructure investment gap brings serious economic consequences such as $3.9 trillion in losses to the U.S. GDP by 2025, $7 trillion in lost business sales by 2025, and $2.5 million lost American jobs in 2025. There is a clear pressing need to invest in our nation’s infrastructure. With over 50,000 state and local governments and entities able to issue tax-exempt bonds for key infrastructure projects, these important municipal finance tools can ease the burden on the American taxpayer while also bolstering investment in critical public needs, enhancing the quality of life of all Americans. Proceeds directly fund infrastructure and governmental activities by reducing state and local government borrowing costs and providing an incentive for public investment in infrastructure and other facilities.

SIFMA supports a number of initiatives related to municipal finance, including reinstating the tax exemption for advance refunding bonds; authorizing a new direct pay bond program on a permanent basis as a supplement to, not a replacement for, tax-exempt bonds; permitting state and local governments to issue tax-exempt bonds for infrastructure projects with private participation in the same manner that they issue bonds for purely public projects, and also expanding the volume cap and permitted uses of private activity bonds (PABs); and expanding the number of “bank-qualified” bonds from the current limit of $10 million to $30 million with inflation adjustments for future years.

Equity Market Structure and Market Data

www.sifma.org/equity-market-structureThe evolution of equity market structure – including pilot programs, capital formation, market data and self regulatory organization (SRO) structure – is a key priority for SIFMA.

Market data is information about current stock prices, recent trades, and supply-and-demand levels sold by national securities exchanges. Access to this information is essential to America’s world-leading capital markets because retail investors and market professionals need the most complete and up-to-date market information possible to make informed investing and order routing decisions. Because exchanges control that information, they have enormous pricing power over the cost to access the data. This data is distributed exclusively by exchanges in a two-tier system comprised of a public feed – the Securities Information Processor (SIP) – that distributes “best-priced” quotation and “last-sale” data for securities, and faster proprietary data products that include additional information, such as “depth-of-book” information that shows all other bid offers. Because exchanges control both tiers of information, they have enormous pricing power over the cost to access the data. As a result, the SIP has lagged proprietary data feeds in providing critical information at sufficient speeds and there have been massive increases in fees for market data in recent years.

In June 2020, the Securities and Exchange Commission and the U.S. Justice Department announced they would partner in efforts to review the fees the exchanges charge for data. SIFMA welcomes this initiative and believes the agreement should allow the SEC to determine whether exchange fees are subject to competition. SIFMA has long argued that these fee increases are inconsistent with the exchanges’ actual costs in collecting and distributing market data and thus constitute an excessive mark-up over cost. The SEC is also developing a new single national market system plan governing the public dissemination of real-time consolidated equity market data for national market system (NMS) stocks. Known as the CT Plan, this will consolidate three current market data plans into a single plan to govern the distribution of equity market data, reducing duplication between the plans and eliminating exchanges’ conflicts of interest as operators of the SIPs. In December 2020, the SEC announced its adoption of market data infrastructure rules under Regulation NMS. SIFMA strongly supports the SEC’s unanimous approval of its infrastructure proposal, as it is a positive step to provide investors with critical additional market data and to address current conflicts of interests for exchanges between the SIP data and exchange proprietary feeds.

Market data reform should focus on promoting competition, supporting efficient markets, and providing a transparent and fair system for all investors.

Financing Sustainability

www.sifma.org/esgEnvironmental, Social, and Governance (ESG) refers to a broad range of non-financial factors on which socially conscious investors assess the sustainability and societal impact of their potential investments in a company. Environmental is how a company performs as a steward of nature; social is how they manage relationships with the communities where they operate; and governance is their leadership, executive pay, shareholder rights and more.

ESG is increasingly shaping the way investors choose to engage with companies and thus how companies do business around the world. As investors have shown an interest in putting their money where their values are, brokerage firms and mutual fund companies have significantly increased their offerings of exchange-traded funds (ETFs) and other financial products to support investor and client needs.

SIFMA and SIFMA’s Asset Management Group (AMG) are working closely with our partners at the Global Financial Markets Association (GFMA) on issues like accelerating the evolution of capital markets’ Climate Finance Market Structure (CFMS) and providing market insights as regulators around the world develop standards to support mobilization of capital for climate finance. SIFMA will continue to work on educational efforts regarding ESG investing in the U.S. and abroad.

A $100-150T Investment Need: Climate Finance Markets and the Real Economy

www.gfma.org

Climate change poses economic and financial risks to the global economy. In order to transition to a low carbon economy, climate finance market structure must grow at an unprecedented scale, speed, and geographic scope to meet the projected $100-150 trillion investment need.

Climate Finance Markets and the Real Economy – a report co-authored by SIFMA’s global affiliate, the Global Financial Markets Association (GFMA), and Boston Consulting Group (BCG) – is a call to action for coordinated and concerted action by the public, social, and private sectors to significantly scale the climate finance market structure over the next three decades. These include a call for evolving our current market structure to address the advent and needs of climate finance and the creation of financial instruments and structures required to continue to serve the financing, investment and risk management needs for a broad set of market participants, as well as market wide sector, or individual corporate, and region-specific changes necessary to motivate investment. The report also highlights the role that capital markets and other participants must play to support transition pathways at the same time continue to serve their clients, investors, and the societies where they want to do business.

Transitioning from LIBOR to Alternative Reference Rates

www.sifma.org/liborThe financial industry and global regulators are transitioning from LIBOR to more robust alternative reference rates. LIBOR is the most commonly used benchmark for short-term interest rates, often referenced globally in derivative, bond and loan documentation. It is estimated that $200 trillion of financial contracts and securities are tied to USD LIBOR and that matters to everyone – small businesses, corporations, banks, broker dealers, consumers, and investors. Market participants are transitioning away from LIBOR, because it is based on relatively few transactions and relies heavily on expert judgment in determining the rate. The scarcity of underlying transactions makes LIBOR potentially unsustainable, as banks may eventually choose to stop submitting altogether. The transition from LIBOR to alternative interest rate benchmarks is well underway, but much work lies ahead.

The Financial Conduct Authority (FCA), the regulator of LIBOR, has announced it will no longer compel banks to submit LIBOR quotes after 2021, raising the possibility that LIBOR may be deemed unrepresentative and/or cease publication after that time. Indeed, the administrator of LIBOR, ICE Benchmark Administration, announced that it will consult on ceasing production of a number of flavors of LIBOR, including U.S. dollar LIBORs. In the U.S., regulators have supported a plan to stop using LIBOR on new transactions by the end of 2021 while backing a plan to allow many existing transactions to mature before LIBOR fully winds down in June 2023. This makes it imperative for financial market participants and end users to prepare for a time – coming in short order – when they will not be able to use LIBOR as a benchmark for new products, and will need to shift legacy instruments to alternative rates.

SIFMA and our partners at the Global Financial Markets Association (GFMA) were early proponents of global reform efforts with the November 2012 publication of Principles for Financial Benchmarks. Since that time, we have engaged with and are supportive of efforts by global regulatory bodies related to market standards and principles for benchmarks. In June 2017, the Federal Reserve’s Alternative Reference Rate Committee (ARRC) selected the Secured Overnight Funding Rate (SOFR) as the rate that, in its consensus view, represents best practice for use in certain new U.S. dollar derivatives and other financial contracts.

SIFMA is committed to working in close cooperation with the industry, U.S. and global regulators, and trade associations as a member of the Federal Reserve’s Alternative Reference Rate Committee (ARRC). Issues SIFMA is focused on include: legacy transactions, implementation of robust fallback provisions, and development of term rates in support of a successful transition to alternative reference rates.

The SOFR Primer

www.sifma.org/sofr-primer

In this primer from SIFMA Insights, we provide an overview of the LIBOR transition, with a focus on the proposed U.S. alternative reference rate, the Secured Overnight Financing Rate (SOFR). SOFR is based on the overnight repo markets, moving the reference rate from being based on ~$1 billion transactions per day (the most active tenor of LIBOR, three months) to the repo market with around $1 trillion of transactions per day. Publication of the SOFR rate began in April 2018; trading and clearing of SOFRbased swaps and futures began in May 2018.

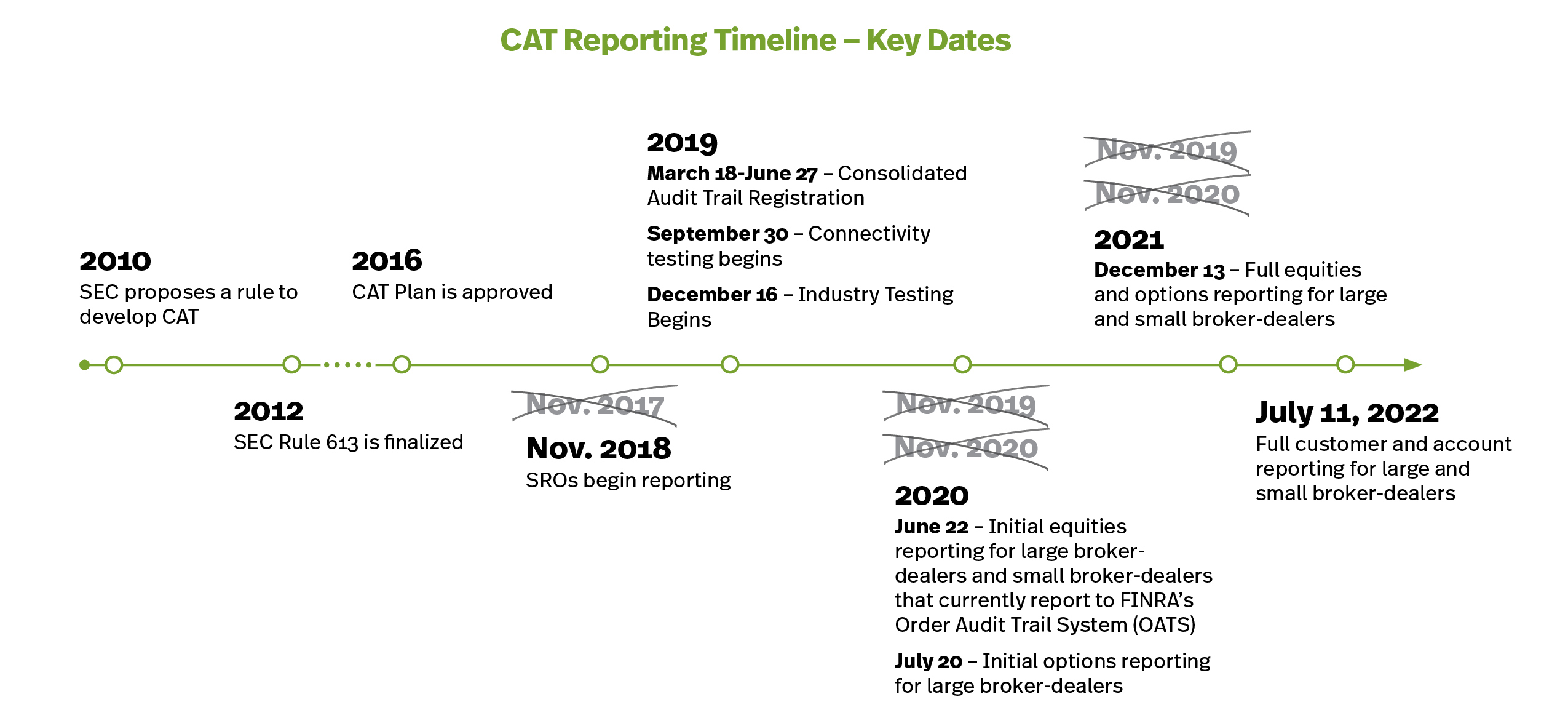

Implementing the Consolidated Audit Trail

www.sifma.org/catThe SEC and the self regulatory organizations (SROs) continue to develop a comprehensive Consolidated Audit Trail (CAT) that would enable regulators to track all activity throughout the U.S. for equities and options trades.

The CAT will allow regulators to link every order through its entire life cycle, including cancellations, modifications and executions, and the CAT database will link all orders with the account holder. As such, the CAT will enable regulators to conduct cross-market surveillance and market reconstruction by pulling together detailed trading data from all market centers.

SIFMA advocates for a secure system that expedites the retirement of duplicative systems, while promoting an inclusive governance structure and equitable funding model. SIFMA has expressed concerns around risks related to the collection of Personally Identifiable Information (PII) within the CAT and worked with the SEC and the SRO’s as they make significant steps forward in holding the CAT to the highest security standards.

Digitalization and Security Tokens

www.sifma.org/security-tokensU.S. capital markets have continued to innovate as technology has allowed for profound evolutions in market infrastructure, changing at times the very nature of American financial markets. Distributed ledger technology (DLT) and the potential benefit it may bring to the capital market ecosystem and infrastructure are a key topic of interest amongst market participants.

SIFMA and PricewaterhouseCoopers LLP published a paper, Security Tokens: Current Regulatory and Operational Considerations for Broker-Dealers and a Look Towards the Future. The paper provides a foundational understanding of how DLT and digital assets such as security tokens can offer new and cost-efficient methods of capital formation. It also describes the key operational challenges faced by U.S. broker-dealers hoping to adopt this technology and recommends where regulatory clarity would be helpful in addressing these challenges. SIFMA developed the paper in collaboration with its member working groups, and determined and identified the activities, requirements, and considerations for market participants engaging in operationalizing security tokens.

Security tokens are securities issued solely on DLT that satisfy the applicable regulatory definition of a security or financial instrument under local law and/or a token that represents on DLT underlying securities/financial instruments issued on a different platform, where such representation itself satisfies the definition of a security/financial instrument under local law. There are a number of issues across the lifecycle of a security to consider, some of which must be addressed by stakeholders and regulators for the market to fully develop. The goal is to embrace innovation that creates efficient market structures while still providing the same investor protections that we have built up over decades.

As the industry moves forward with the broader adoption of these assets and their supporting technology, SIFMA believes dialogue between industry participants and regulators will help support the further growth of the markets for the security tokens and the adoption of the technology that supports them.

Helping Businesses and Investors Manage Risk

www.sifma.org/derivativesTitle VII of the Dodd Frank Act established a broad new regulatory regime for over-the-counter (OTC) derivatives, or swaps, which is profoundly affecting the financial markets and market participants. Sufficiently liquid and standard swaps are subject to mandatory clearing, which requires transactions to be submitted to a central counterparty. Further, certain cleared transactions are required to be executed on electronic trading platforms, such as swap execution facilities or designated contract markets. However, some swaps will appropriately remain bilaterally cleared and/or traded.

SIFMA believes that the Dodd-Frank Act took several important and necessary steps towards improving oversight and transparency in the swaps markets and supports the implementation of appropriate regulations that do not create undue costs or unduly limit the availability of these valuable risk management tools for American businesses.

Policymakers should consider the following to help achieve these objectives:

Regulatory Harmonization: The SEC and CFTC should continue to harmonize their final rules and regulations for swaps and security-based swaps.

SEC Title VII Implementation: The SEC’s security-based swap dealer (SBSD) regime is poised to go live in October 2021, with the first SBSD registrations expected by November 1. SIFMA is working with members on identifying and addressing issues, and engaging with the SEC and FINRA as needed, in areas such as SBSD registration, supervision, compliance, recordkeeping, margin, capital and financial reporting, among others.

Cross Border Application of Title VII Rules: An overly broad application of Title VII rules will result in overlapping, duplicative or conflicting requirements that fragment markets, create competitive disadvantages, and foster opportunities for regulatory arbitrage. Consistent with the intent of Congress, U.S. regulators should apply Title VII rules only where there is a direct and significant connection to the U.S. and, where necessary, extraterritorial application of the rules should provide for substituted compliance in comparable jurisdictions.

Margin Requirements for Non-Centrally Cleared Derivatives: SIFMA continues to advocate for regulators to take an internationally coordinated and workable approach to the implementation of margin requirements for non-centrally cleared derivatives, in accordance with the globally agreed framework issued by the Basel Committee on Banking Supervision and IOSCO.

Helping More Americans Save for Retirement

www.sifma.org/retirement-legislationSIFMA supports the Securing a Strong Retirement Act 0f 2020 (SECURE Act), introduced by House Ways and Means Committee Chairman Richard E. Neal (D-MA) and Ranking Member Kevin Brady (R-TX). The bill represents important steps toward enhancing the private retirement system and increasing retirement savings. It includes provisions that will incentivize small business to offer retirement plans, enable older Americans to save more and hold on to their savings longer, and allow matching contributions for student loan payments.

Catch-up Contribution Limit: Many Americans have taken hardship loans or distributions from their retirement accounts to pay for living expenses during the coronavirus pandemic. The SECURE Act includes provisions that would index the IRA catch-up contribution limit for savers over 50 and raise the catch-up limit for those over 60.

Due to market volatility and economic turmoil attributable to COVID-19, individuals need the flexibility to be able to make additional contributions and make-up for the losses to their retirement savings from the pandemic. These workers, nearing retirement age, have less time to replenish their savings, and SIFMA supports a permanent increase for this limit to empower Americans to assess their financial security and re-build their savings. This proposal is included in both the Portman Cardin retirement package, as well as Chairman Neal’s and Ranking Member Brady’s SECURE Act.

Required Minimum Distribution (RMD) Relief: SIFMA supports improving RMDs to help retirement savings last longer for retirees. The Securing a Strong Retirement Act includes several provisions related to improving RMDs: increasing the RMD age to 75 and holding harmless RMDs for individuals with balances under $100,000.

The economic effects of the COVID-19 pandemic has caused a lot of financial uncertainty for many and their savings. In the Coronavirus Aid, Relief, and Economic Security (CARES) Act, Congress recognized this uncertainty and included a freeze for RMDs for 2020. Retired Americans who have been saving their whole working lives should be allowed to let their money benefit from an economic recovery at a time when their health and financial security is at enormous risk. Our firms need as much time as possible to operationalize these changes to the RMD program and communicate with their clients about the options available to them. SIFMA supports a further RMD freeze for 2021 given the ongoing economic uncertainty of the pandemic.

Employer Match for Student Loans: Retirement savings is just one part of financial wellness. For many young people, paying student loans is a real challenge and a top priority. The IRS, through a private letter, authorized an employer to match an employee’s retirement plan when they pay off their student loans, allowing an employee to pay off their loan while their employer helps them begin saving towards retirement. SIFMA supports allowing all employers to provide this match program, because the sooner the employee can start saving, the better set they will be for the future. There is bipartisan support to codify the IRA action via legislation: S. 1428: Retirement Parity for Student Loans Act and H.R 6276: Retirement Parity for Student Loans Act.

Enhancing Investor Protection While Preserving Choice

www.sifma.org/reg-biRegulation Best Interest – finalized by the Securities and Exchange Commission in 2019 and fully enforceable as of June 2020 – significantly and meaningfully upgrades the existing regulatory regime for broker-dealers, and directly enhances investor protection. SIFMA advocated for the creation of such a standard for over a decade.

The rule is specific with respect to the obligations brokers owe to their clients and the steps they must take to comply, including the obligation to eliminate, disclose and mitigate certain conflicts of interest. It is enhancing investor protections, while also preserving investor choice and access to investment advice.

Reg BI substantially exceeds the preceding FINRA suitability standard and is broader in scope than the now defunct DOL fiduciary rule. Reg BI applies across all customer accounts, not just retirement accounts, and will allow the SEC to enforce a common standard across the industry. Attempts by Congress to weaken Reg BI would hurt investor protections implemented by brokers.

Reg BI Implementation Survey

A survey of wealth management firms, conducted by SIFMA and Deloitte, regarding the implementation of the SEC’s Regulation Best Interest found that as a result of the regulation, firms made changes to their business models and have prioritized the management of conflicts of interest, strengthened their compliance systems and procedures, and invested significant resources while providing meaningful

protections. Across the 20 survey participants, approximately $114 million has been allocated to readiness efforts.

Safeguarding Investor Privacy

www.sifma.org/privacy-data-protectionSIFMA supports data privacy policies, which take into account existing, strong Federal rules under the GrammLeach-Bliley Act that ensure firms maintain privacy in their client relations and transparency in how data is being used and protected.

Data privacy is a top priority for financial firms. Investors are increasingly looking for transparency as they determine how their data is being used and how it is being protected. SIFMA supports a federal privacy framework that would preempt state law, as many of our firms function regionally, nationally, and globally. In financial services, the Gramm-Leach-Bliley Act, has served as the cornerstone for the industry’s data privacy framework.

Should there be a change to how data privacy is handled at the federal level, it is critical that any framework take into consideration how changes to privacy law would affect the Gramm-Leach-Bliley Act.

Privacy & Data Aggregation

Personal financial information is invaluable and the financial industry is committed to ensuring the safety of the clients we serve at every turn. SIFMA believes a federal privacy and data breach standard is necessary to best protect the personal financial data of all Americans. SIFMA is a founding member and serves on the Board of the Financial Data Exchange (FDX), a subsidiary of FS-ISAC tasked with developing technical solutions for secure data aggregation.

Building the Independent Contractor Model

www.sifma.org/independent-contractorSIFMA supports preservation of the independent contractor status in the financial services industry where independent broker-dealer and independent financial advisors can provide services to their retail and institutional clients.

The gig economy has changed the labor landscape in the United States drastically in recent years. Many of these workers are classified as independent contractors under the National Labor Relations Act (NLRA). There is debate as to whether this is an appropriate classification for those workers; however, in the financial services industry, many brokers and advisors choose to operate as independent contractors.

Independent broker-dealers (IBDs) and the nearly 160,000 individuals that affiliate with them as independent financial advisors (IFAs) serve millions of clients across the U.S. by providing investment advice and education.

IFAs provide crucial advice on retirement planning, educational funding, and other life events retail investors in addition to offering other services and products, such as insurance and tax planning, that address their clients’ financial well-being holistically.

Independent contractor status allows independent financial advisors to own and operate their own small business. Independent financial advisors also benefit from a decentralized business structure, which expands the accessibility of financial advice and planning in parts of the country that would otherwise not be served. Notably, independent financial advisors work in a highly regulated industry and are required by securities laws to associate with a broker-dealer to protect investors.

In 2019, California enacted a new worker classification law. It, however, avoided the unintended consequences of capturing traditional independent contractor models like ours by exempting the securities and insurance industries, realtors, doctors, and direct sales agents among others from the law’s purview. We encourage lawmakers to exempt independent broker dealers and independent financial advisors from any legislation that would prevent financial services professionals from freely choosing to be independent contractors.

Tax Policy Supporting Economic Growth

www.sifma.org/taxTaxes impact the savings and investment decisions of individuals and corporations and are a necessary means for funding the government. SIFMA believes reasonable taxation and economic growth are not mutually exclusive and encourages policy makers to consider both when contemplating changes to the tax code. Many of SIFMA’s members are global taxpayers as well, therefore international standards for raising revenue should consider the highly regulated nature of the financial services industry. SIFMA’s member firms are willing and prepared to help policymakers wade through the nuances and goals of their respective tax policy.

Capital Gains and Dividends

Dividends are payments made by a corporation to an individual who owns the corporation’s stocks. Investors who receive dividends must pay taxes on them through their personal income taxes. The dividend tax paid by investors is the second time taxes are paid on that income, hence the dividend tax is a double tax. First, a corporation pays taxes on its profits and pays dividends from what remains. Once the dividend is received by an individual, the stockholder pays a second tax on that same money through their person income tax filing.

The U.S. has one of the highest tax burdens on dividends in the world. Of the 25 million tax returns with dividends, 63 percent are from taxpayers age 50 and older, and 68 percent are from returns with incomes less than $100,000. Increasing the dividend tax would make the U.S. system of double taxation on corporate profits and dividends worse and continue to hamper U.S. competitiveness. Increasing the dividend tax does nothing more than disincentivize investments in these dividend paying companies, which are often the most stable American strongholds that employ union employees, provide health care, and provide pensions for their employees.

Devaluing an investment in these companies would reduce stock prices, ultimately hurting the overall value of companies and continuing to hamper any chance they have at being competitive.

Financial Transaction Tax

A financial transaction tax (FTT) is essentially a sales tax on investors. They tax trades in the amount of a fraction of a percent, and the costs are passed along to investors and savers. Taxing savings and retirement vehicles runs counter to many longstanding policies promoting savings and economic growth, and the negative impact on the world’s most liquid market is of further detriment to all investors.

FTTs in general reduce the return on investment savings and could require many middle- and lower-income citizens to significantly delay their retirement. For example, a Vanguard analysis shows the cost to an individual saving for retirement, who invests $10,000 per year over 40 years in a balanced portfolio of actively managed stocks (60%) and bonds (40%), with a 10-basis point FTT imposed on purchases of securities would be some $36,000—more than 3 ½ years of annual savings. Moreover, in jurisdictions where FTTs have been implemented, they have consistently lowered trading volumes and hurt liquidity.

Examining the Interplay of Finance and International Policy

www.sifma.org/international-policyModern capital markets operate in an inherently cross-border framework. SIFMA supports an open, rules based, global economy in which financial services can do its part to boost exports, investment and global economic growth.

Data: In the 21st century, the ability to transfer data across borders and locate servers where needed is crucial for U.S. financial services firms operating globally. Unfortunately, many countries have implemented data localization policies that hinder the free flow of data, imposing economic costs both on the industry and the GDP of countries pursuing such regulations. The United States-Mexico-Canada Agreement (USMCA) included a prohibition on forced data localization, which also granted regulators necessary access. Future trade and investment agreements should include provisions to ensure the free flow of data.

U.S.-China Economic Relationship: SIFMA supports efforts to open China’s financial markets to U.S. and other non-Chinese participants. This was a key component of the U.S. and China’s Phase One trade agreement and SIFMA believes that China should fully deliver on this commitment with the following actions: remove the foreign equity cap in the life, pension, and health insurance sectors and allow wholly U.S.-owned insurance companies to participate in these sectors; and eliminate foreign equity limits and allow wholly U.S.-owned services suppliers to participate in the securities, fund management, and futures sectors.

U.S.-UK Trade and Regulatory Cooperation: A future U.S.-UK trade agreement offers an unprecedented opportunity for putting financial services at the heart of a new economic relationship while enhancing the economic benefits to both countries. The future relationship between the U.S. and UK in financial services, through a trade and investment agreement, should aim to have four key characteristics: ensure that both economies maximize opportunities for exports and cross-border investment in financial services, integrating the U.S.-UK market in financial services and strengthening the competitive advantage of the industry in both the UK and U.S.; be forward looking and transparent and designed to tackle regulatory frictions early in the rule-making process; strengthen the UK and U.S. as leading influencers of the future international financial regulatory agenda as rule setters; and help re-define how trade and investment agreements are conceived, by fully integrating services and addressing truly 21st century challenges arising from modern technology and cross-border operations.

Prudential Regulation of the Capital Markets

www.sifma.org/prudential-regulationPrudential regulation requires financial firms to control risks, hold adequate capital and liquidity, and have in place workable recovery and resolution plans. It is essential that our regulatory regime accounts for the vital role the capital markets play in providing credit and financing the real economy.

SIFMA supports appropriate regulation of the capital markets and their participants by both market regulators, who have decades of experience in promulgating rules and supervising the marketplace, as well as prudential regulators. Unfortunately, too often these prudential rules treat capital markets activities as riskier than commercial lending activities without evidence to support this position taken by the prudential regulators. U.S. prudential rules generally impose significantly higher capital and liquidity costs on banking entities with significant capital markets operations. This has increased costs to financial firms and the economy as a whole and reduced market depth for a wide variety of corporations and other end-users, particularly during periods of economic stress. This has also had another effect: transforming U.S. banking regulators into the most impactful supervisor of the capital markets superseding the oversight role traditionally played by the SEC and CFTC. This has created distortions in the capital and liquidity requirements between market and prudential regulators as well as lessened the efficiencies by increasing costs to end users.

US Risk-Based Capital and Global Basel Standards

There remains substantial capital markets regulations in the form of the Basel end package which will be promulgated only by the U.S. federal banking regulators. The impact of these new regulations is not fully known as the U.S. has yet to publish a notice of proposed rulemaking (NPR) for the Fundamental Review of the Trading Book including Credit Valuation Adjustments or the revisions. However, should the Basel Framework be largely adopted in the U.S., it is expected that capital requirements in terms of Risk Weighted Assets will dramatically increase. It is critical that the U.S. banking supervisors carefully review and analyze the implication of such a needlessly conservative and frankly unduly complex rule on the efficiency and function of the U.S. capital markets.

Non-Bank Financial Intermediation

In November 2020, the Financial Stability Board (FSB) published its Holistic Review of the March Market Turmoil and an accompanying work program on non-bank financial intermediation (NBFI) that will take place between 2021 and 2022. The work program will focus on areas including resiliency of money market funds (MMFs) and open-ended funds, government and corporate bond markets, the impact of post-financial crisis prudential regulation, and margining practices of CCPs. SIFMA will actively engage with key domestic and international policymakers on the issues raised by the work program.