SIFMA’s thought leadership, advocacy and support truly enhance the ability of its member firms to serve clients at the highest level.

James R. Allen

Vice Chairman, Robert W. Baird & Co. Incorporated 2019 Chair, SIFMA Board of Directors

The financial industry and markets are in an extended period of dramatic change. Technology is revolutionizing the industry, that is indeed true, but a confluence of several major events is actually behind our seismic shift. The industry is still absorbing new regulations to ensure safety and soundness, but finding our ability to facilitate capital formation and economic growth is often constrained by it. The skills needed for today’s workforce are changing and we are investing in our people to ensure they can grow with our firms. We are striving to foster a diverse and inclusive industry, with our professionals representative of our clients and our culture welcoming to all. The way we serve the individual investor is changing, too, with technology supporting our ability to focus on holistic wealth planning.

It all comes back to what we do: bringing capital to the best ideas and enterprises, and bringing investment opportunities to retail and institutional investors.

Prudential Regulation

Since the crisis, the financial industry has built up significant capital to enhance the resiliency of the financial system.A proxy for the entire financial system, firms subject to the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR) now have more than $1 trillion of Common Equity Tier 1 capital (CET1) – an increase of 71% since 2009. Their average CET1 ratio is 11.8%, well above the 7% minimum requirement and even greater than the maximum regulatory requirement inclusive of the highest G-SIB surcharge. It is also estimated that, for the largest financial institutions, increases in capital and the introduction of convertible long-term debt as required by the TLAC rule has substantially increased total loss bearing capacity from roughly 15% in 2008 to more than 25% in 2018.

I believe it is prudent to review all “our practices to ensure that they are as efficient and transparent as possible and that they remain appropriate in light of changes in the industry that have been achieved.

Randal K. Quarles

Vice Chair for Supervision, Federal Reserve Board of Governors Chair, Financial Stability Board July 2019

With the adoption of numerous conservative prudential regulatory requirements, banks now hold excessive levels of capital and liquidity that are increasingly disconnected from the level of risk they incur. Although these levels have undoubtedly increased resiliency, they come at a cost: the more capital required, the less deployed into the economy.

Prudential and market regulators have set out to tailor and improve upon the post-crisis regulatory regime, executing on recommendations put forth by the Treasury Department to rebalance and modernize financial regulation. To that end, industry and regulators have been examining recalibrations to several major rules adopted over the last ten years.

Policymakers and regulators should take steps to ensure prudential regulations promote the stability of the financial system but do not negatively impact capital formation and economic growth, notably Basel provisions, including:

- Standardized approach for counterparty credit risk (SA-CCR);

- Supplementary leverage ratio (SLR) and enhanced supplementary leverage ratio (eSLR);

- CCAR requirements;

- Stress capital buffer (SCB) requirements; and

- Fundamental review of the trading book (FRTB).

Are CCAR Shocks to the Trading Book Plausible?

www.sifma.org/gms-lcd-study

A September 2019 study using statistical analysis of stress testing scenarios concludes that, in a number of significant areas, GMS/LCD shocks are not reasonably plausible and it is, therefore, important to revisit key aspects of CCAR.

Capital Markets

Market Data

Market data is information about current stock prices, recent trades, and supply-and-demand levels sold by national securities exchanges. Access to this information is essential to America’s world-leading capital markets, because all participants need timely and complete data to make informed trading decisions. Because exchanges control that information, they have enormous pricing power over the cost to access the data.

At SIFMA, we believe market data reform should focus on promoting competition, supporting efficient markets, and providing a transparent and fair system for all investors. We continue to advocate for improvements to the SIP content, consistent with the recommendations the SEC is developing for proposals to changes to the SIP, and for the addition of competing SIPs to replace single-consolidator model.

Housing Finance Reform

The U.S. housing market is a critical piece of the general economy. It represents one-fifth of U.S. GDP and 35% of all private, non-financial debt in the country.

In March 2019, a Presidential Memorandum was issued for Federal Housing Finance Reform that directed the U.S. Department of the Treasury and the Department of Housing and Urban Development (HUD) to conduct a broad review of our housing finance system, including the Government-Sponsored Enterprises (GSEs), Fannie Mae and Freddie Mac. In September, the Treasury and HUD released their housing finance reform plans. SIFMA supports the U.S. Administration and Congress working together to identify a permanent solution. Moving the GSEs out of the conservatorship of their regulator, the Federal Housing Finance Agency (FHFA), is a goal that we support – but not without Congress taking the necessary action to address the need for an explicit government guarantee to ensure stable mortgage-backed securities (MBS). In their plans, the Administration outlined both legislative and administrative steps for reform of the GSEs and housing finance. While the outlook for legislation is uncertain, it is clear that the Administration intends to take administrative steps toward reform.

The Volcker Rule

While pure proprietary trading for one’s own account was historically a limited activity for most banks, the ability to trade and take positions in securities has been an essential tool to making markets and ensuring those markets remain liquid.

SIFMA supports the regulatory agencies’ goal of reducing compliance-related inefficiencies of the Volcker Rule. Revisions issued in August 2019 will help ensure the Rule does not negatively impact capital formation and economic growth, which could exacerbate financial harm during times of stress. The removal of the accounting prong is a positive step forward in ensuring the regulatory definition of ‘trading account’ does not go beyond the statutory definition and Congressional intent. In the face of studies showing the Rule’s negative impact on liquidity, including from the Office of Financial Research, and numerous calls to simplify the Rule, including from former Fed Governor Dan Tarullo and Paul Volcker, it was clear revisions were needed. It is important to be clear on what the changes encompass: the prohibition on proprietary trading under the Rule is statutory and will not go away. However, the revisions do provide market participants with more clarity on compliance as they implement the continuing legal restrictions under the Rule, and they will make it easier for the regulators to ensure compliance.

The next step in the process is for the agencies to finalize matters pertaining to the covered funds provisions of the Volcker Rule. SIFMA would like to see clarification around certain related definitions as well as exclusions for specific vehicles that we do not believe represent proprietary trading and therefore should not be included in prohibitions.

Wealth Management

Regulation Best Interest Implementation

In June, the SEC voted 3-1 to adopt Regulation Best Interest. Reg BI requires broker-dealers to act in the best interest of their retail customers when making a recommendation of any securities transaction or investment strategy involving securities to a retail customer. The SEC also adopted Form CRS, a customer relationship summary. Finally, the SEC also issued interpretive guidance regarding the broker-dealer exclusion from the definition of investment advisers, and interpretive guidance regarding the standard of conduct for investment advisers.

Since early 2009, SIFMA has consistently advocated for the establishment of a best interest standard for financial professionals when providing investment advice. For that reason, we have supported the efforts of the SEC to finalize comprehensive federal regulations that meaningfully raise the bar for broker-dealers when providing personalized investment advice about securities to retail customers. While well-intentioned,

a patchwork of state-by-state approaches currently under discussion would undermine the new federal standard and also the interest of investor protection generally.

To assist firms in understanding the various Reg BI and Form CRS requirements and their potential impacts, SIFMA partnered with Deloitte to develop a Reg BI implementation guide as a high-level framework for compliance and for assessing the rule’s potential impacts on firms.

As written, the SEC’s Regulation Best Interest rule imposes a materially heightened standard of conduct for broker-dealers when serving retail clients. While principles- based, the rule is specific with respect to the duty and obligations brokers owe to their clients, and what steps they must take to comply, including the obligation to eliminate, or disclose and mitigate, certain conflicts of interest. It is undeniable that this rule will directly enhance investor protection and contribute to increased professionalism among financial service providers. Compliance with the rule will not be easy for the industry. Firms will need to make substantial changes. The costs to implement will no doubt be significant, but, we believe, worthwhile to uniformly enhance investor protection to the level investors should and do expect, while preserving investor choice and access to investment advice.

Kenneth E. Bentsen, Jr., President and CEO, SIFMA

June 2019

Senior Investor Protection

It is vital that we are able to protect our senior investors from financial exploitation and the dangers of cognitive decline. SIFMA has been working with industry members, academics, and state and federal lawmakers to advance policies, practices, rules, regulations and statutes which enhance senior investor protections.

A growing number of states have enacted senior investor protection laws that extend to broker-dealers, and several others are currently working to develop a similar path. Additionally, FINRA Rule 2165, permitting pauses on certain suspicious activity, and FINRA Rule 4512, requiring firms to request trusted contact information from certain clients, went into effect in February 2018. SIFMA continues to push for updated laws and regulations to get ahead of this emerging threat and better equip advisors – through regional workshops, toolkits and more – to protect their aging client base. This is an issue of increasing importance, and SIFMA looks to continue to lead on this issue, as it has for the past several years.

Retirement Savings Legislation

The retirement system in the United States is helping millions of Americans save for a secure retirement and maintain their standards of living as retirees. However, increased life expectancies, the uncertain future of Social Security benefits, higher health care costs, and low interest rates have increased the need for American workers to save more for retirement.

Since its inception, the retirement system has become more effective and portable, leading to increased financial security for many Americans. Retirement savings plans also play an important role in the capital markets, as the contributions from these plans form a large amount of the capital invested in our financial markets.

SIFMA is committed to increasing retirement security and has identified three primary pillars to reach this goal:

- Expanding access to plans,

- Increasing participation and decreasing leakage, and

- Enhancing education.

SIFMA encourages passage of retirement legislation that includes Open MEPs, increased incentives for small businesses to open plans, an increase in the RMD age, along with other provisions to improve access to retirement savings.

Tax Policy

A Financial Transaction Tax

A financial transaction tax (FTT) is a levy on transactions of stocks, bonds and derivatives. While proposed as a means to raise funds or curb behavior, a financial transaction tax amounts to a sales tax on investors, savers and retirees.

SIFMA is strongly opposed to a financial transaction tax, which raises costs to the issuers, pensions and investors who help drive economic growth, negatively impacting those saving for retirement, college or to buy a home by decreasing the amount of their savings. Moreover, major economies that have adopted such taxes have had overwhelmingly negative results, including reduced asset prices, trading moving to other venues, market dislocation and decreased liquidity. Past experience also suggests that it would raise less revenue than supporters often claim.

The U.S. financial markets are the broadest and deepest in the world and this benefits American individuals and businesses in many ways. An FTT would substantially reduce market liquidity and impair the strength of the U.S. capital markets, a move that runs counter to strong, sustainable, and balanced growth, and the financial impact of such a tax is not just on markets.

The Ramifications of a Financial Transaction Tax

www.sifma.org/ftt-ramifications

In October 2019, SIFMA Insights uses failed case studies from across the globe to assess the potential ramifications of a financial transaction tax on capital markets and individual investors.

Tax Reform

The Tax Cuts and Jobs Act (TCJA) significantly changed the way U.S. multinational foreign profits are taxed. Importantly, while the Global Intangible Low Tax Income (GILTI) regime was introduced as an outbound anti- base erosion provision, it has not worked as envisioned. SIFMA supports final regulations that account for the unique concerns of financial services companies, results in the lowest possible effective tax rate on foreign earnings, mitigates the unintended consequences caused by interest expense allocation rules, and obtains reasonable treatment for US branches operating in foreign jurisdictions.

Similarly, SIFMA also supports final regulations for Base Erosion and Anti-abuse Tax (BEAT) and tax-deductible interest that mitigate the impact of taxable interest on inter-company debt. This change would also better reflect the original intent of Congress.

Finally, the TCJA imposed a new limitation on the deduction for business interest expense also known as the 163(j) limitation. SIFMA is in favor of final regulations that ensures interest is not imputed on certain types of uncleared swaps.

Trade Policy

The United States exports over $100bn of financial services a year. SIFMA supports an open, rules based, global economy in which financial services can do its part to boost exports, investment and global economic growth. SIFMA believes that trade agreements should be comprehensive, broaden market access for financial services firms, and address issues specific to today’s economy in digital trade to enhance U.S. economic competitiveness in the 21st century. To that end, we encourage policymakers to: expand the free flow of goods and services around the world and maximize cross-border investment opportunities; coordinate regulatory approaches across borders to ensure a level playing field for domestic and international firms; and address the rise of impediments to the free flow of data.- SIFMA supports efforts to strengthen the U.S.-China economic relationship including by establishing a level playing field in China’s financial markets for all participants, including U.S. firms.

- In North America, we strongly support passage of the United States-Mexico-Canada Agreement (USMCA) which would establish a new gold standard for financial services in terms of protecting the data flows crucial for growth and employment.

- In Europe, together with our colleagues at AFME and GFMA, SIFMA believes that an orderly Brexit is crucial to ensure a smooth exit from the EU and transition to future financial services relationships. SIFMA is also the co-chair of the UK-U.S. Financial and Related Professional Services Industry Coalition which works to present industry views on the future U.S./UK relationship.

Operations and Technology

Cybersecurity

Cybersecurity is a top priority in the financial industry to ensure the security of customer assets and information and the efficient, reliable execution of transactions within markets. It is a shared objective that demands an integrated approach but is often complicated with an overlapping patchwork of regulation. In fact, no fewer than 11 federal agencies impose some form of cybersecurity requirements. This is in addition to individual state, SRO and jurisdictional requirements, as well as standards from the National Institute of Standards and Technology (NIST) and International Organization for Standardization (ISO).

As a global industry, all market participants are interconnected and part of the same ecosystem and need to work together to protect the sector as a whole. This year, SIFMA’s Quantum Dawn cybersecurity exercise went global. Together, financial institutions and the sector, as a whole, practiced and improved coordination and communications with key industry and government partners in order to maintain equity market operations in the event of a systemic cyber-attack.

An effective and efficient cybersecurity policy is achieved most easily through harmonized, risk-based global standards that leverage extensive investments already made. The financial industry is committed to furthering the development of industry-wide cybersecurity initiatives that protect our clients and critical business infrastructure, improve data sharing between public and private entities and safeguard customer information. SIFMA is actively engaged in coordinating the effort to support a safe, secure information infrastructure, with cybersecurity resources which provide security of customer information and efficient, reliable execution of transactions. We continually work with industry and government leaders to identify and communicate cybersecurity best practices for firms of all sizes and capabilities, and educate the industry on evolving threats and appropriate responses.

See the Resources section of this book for our exercises, tests and other resources.

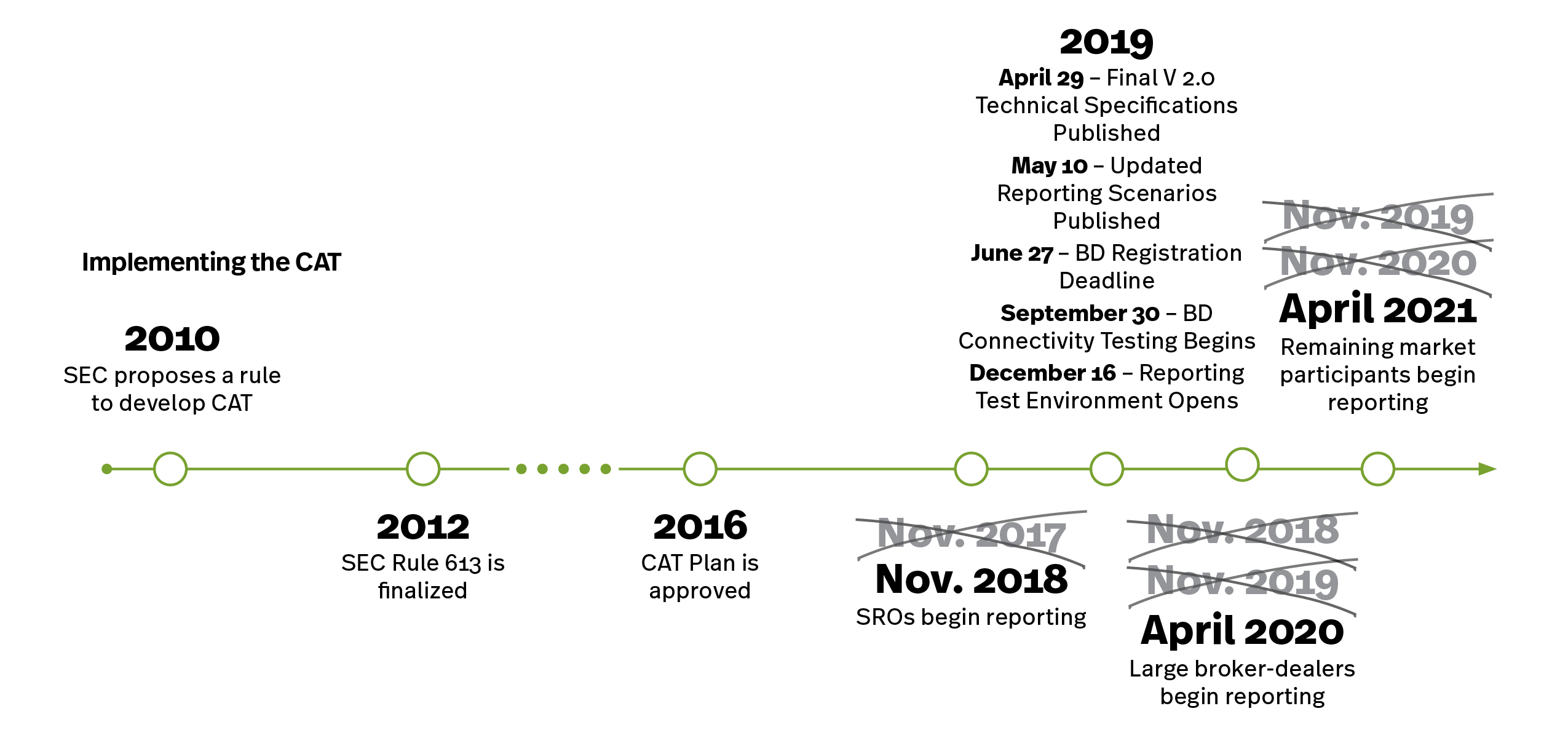

Consolidated Audit Trail

The SEC and the SROs continue to develop a comprehensive Consolidated Audit Trail (CAT) that would enable regulators to efficiently and accurately track all activity throughout the U.S. for equities and options trades.

The CAT will allow regulators to link every order through its entire life cycle, including cancellations, modifications and executions, and the CAT database will link all orders with the account holder. As such, the CAT will enable regulators to conduct cross-market surveillance and market reconstruction by pulling together detailed trading data from all market centers.

SIFMA has focused on concerns around risks related to the collection of Personally Identifiable Information (PII). SIFMA has engaged the SEC and the SRO’s for adjustments to the CAT to ensure adequate data protection and response, as well as restricting access to any submitted data to a strictly controlled environment.

In October, the SROs filed for exemptive relief to remove certain PII – date of birth, SSN and account number – from CAT.

CAT Reporting Timeline – Key Dates

- November 18, 2019: Connectivity Testing Begins

- December 16, 2019: 2a Equities and 2b Options – Industry Testing Begins

- April to October 2020: 2a Equities – Reporting Go Live

- May to December 2020: 2b Options – Reporting Go Live