Reforming Leverage Ratios Is Critically Necessary

Key Points

- U.S. GSIBs must comply with two leverage ratios—the Tier 1 leverage ratio and enhanced supplementary leverage ratio (“eSLR”).

- Binding leverage ratios discourage U.S. GSIBs from holding Treasury securities and intermediating the Treasury market, negatively affecting Treasury market liquidity and resilience.

- Even if the banking regulators were to set the leverage buffer at 50 percent of the GSIB surcharge it will not ease banks’ balance sheet constraints during market stress events like COVID-19’s “dash for cash.”

- By contrast, exempting Treasury securities and central bank reserves from both leverage ratios would incentivize U.S. GSIBs to hold more Treasuries and aid market intermediation.

Background

In December 2017, the Basel Committee issued international standard on leverage ratio framework as part of its Basel III: Finalising post-crisis reforms. The Basel standard envisions that “[t]he leverage ratio is intended to … reinforce the risk-based requirements with a simple, non-risk-based “backstop” measure.” 1 Banks designated as Global Systemically Important Banks (“GSIBs”) must also meet a leverage ratio buffer, set at 50% of their GSIB surcharges. Starting in January 2018, U.S. GSIBs must follow the enhanced supplementary leverage ratio (“eSLR”) rule, requiring a minimum ratio of 3 percent (the “SLR” that is applicable to all large banking organizations) plus a 2 percent leverage buffer. 2 In April 2018, the Federal Reserve Board proposed adjusting the 2 percent buffer to 50 percent of the GSIB surcharge, but this proposal is still pending finalization. 3 Separately, U.S. GSIBs (as well as other large banking organizations) must also comply with Tier 1 leverage ratio of 4 percent, a consequence of the Collins Amendment provisions of the Dodd-Frank Act. Their U.S. insured depository institution (“IDI”) subsidiaries are subject to eSLR of at least 6 percent and Tier 1 leverage ratio of at least 5 percent to be considered well-capitalized.

The unintended binding capital constraint for U.S. GSIBs

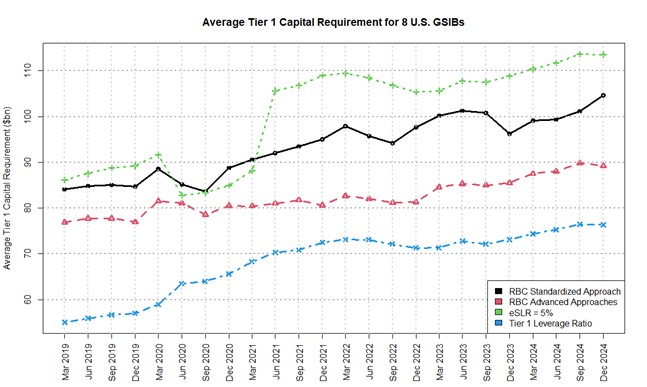

Leverage ratios are designed to serve as a safeguard and backstop against the risk-based capital requirements for U.S. GSIBs. However, in practice, they have frequently been the primary capital constraint for many U.S. GSIBs in recent years. Figure 1 presents the average capital requirements calculated using the two risk-based capital frameworks (the standardized approach and the advanced approaches) and the two leverage ratio frameworks (eSLR and Tier 1 leverage ratio), 4 under the current capital regulations. 5 From March 2019 to December 2024, the eSLR was the primary capital constraint for the eight U.S. GSIBs on average, except between March 2020 and March 2021. During that period, the Federal Reserve Board temporarily exempted Treasuries and central bank reserves from the supplementary leverage ratio to reduce Treasury market strains and support increased lending by large banks during the COVID-19 pandemic. 6

Figure 1. The average dollar amount of risk-based Tier 1 capital requirements of the U.S. GSIBs calculated using both the standardized approach (black solid line) and the advanced approaches (red dashed line), and leverage capital requirements calculated using the enhanced supplementary leverage ratio (green dotted line) and Tier 1 leverage ratio (blue dashed line).

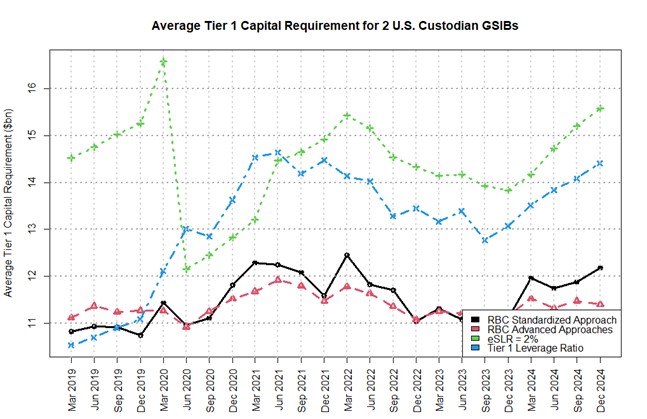

Since the beginning of 2019, leverage ratios have been the binding capital constraints for the two U.S. GSIBs that primarily engaged in custody, safekeeping, and asset servicing activities, as shown in Figure 2. This has remained true even with the above temporary exemption of Treasuries and the permanent exemption of central bank reserves from eSLR, as required by section 402 of the Economic Growth, Regulatory Relief, and Consumer Protection Act. 7 Custody banks perform nearly all financial activities at their IDIs, which are subject to higher eSLR requirements and are therefore more likely to be constrained by eSLR. In addition, central bank reserves remain part of the Tier 1 leverage ratio calculation, which is a significant factor in determining Tier 1 leverage ratio as the binding capital constraint for banks, notably during periods of financial stress due to deposit flows from clients.

Figure 2. The average dollar amount of risk-based Tier 1 capital requirements of 2 U.S. Custodian GSIBs calculated using both the standardized approach (black solid line) and the advanced approaches (red dashed line), and leverage capital requirements calculated using the enhanced supplementary leverage ratio (green dotted line) and Tier 1 leverage ratio (blue dashed line).

This treatment also stands in contrast to other major jurisdictions. For example, the European Central Bank found in its 2024 review that most EU banks have lower leverage-based requirements than risk-based ones, aligning with the Basel leverage ratio framework’s goal. 8

The Group of Thirty’s report, U.S. Treasury Markets: Steps Toward Increased Resilience, suggests that “[w]hen the SLR is binding or even when there is a significant chance that it will be binding in the future, banks are discouraged from allocating capital to relatively low-risk activities because the SLR requires too much capital to support those activities. And market-making in the U.S. Treasury markets is a prime example of a low-risk activity to which banks have been allocating less capital since the SLR was put in place”. 9 In addition to serving as primary dealers, U.S. GSIBs also act as secondary Treasury market intermediaries with banks and non-banks. As such, reforming leverage ratios is critically necessary to ensure U.S. GSIBs can support the expected Treasury issuance surge over the next decade. 10

Options for reforming leverage ratios

The Federal Reserve Board has at least five potential options to align leverage ratios with the Basel leverage ratio framework’s goal. These options include (1) setting the eSLR leverage buffer at 50% of the applicable GSIB surcharge; (2) setting the eSLR leverage buffer at 50% of Method 1 GSIB surcharge; (3) exempting Treasury securities and central bank reserves from leverage ratio calculations across-the-board (akin to the 2020 temporary exemption, but also inclusive of the Tier 1 leverage ratio); (4) making the eSLR leverage buffer countercyclical; and (5) exempting central bank reserves from the supplementary leverage ratio calculations without reducing the total amount of capital. The latter two options were proposed by former Under Secretary of the Treasury for Deomestic Finance Nellie Liang in her testimony before the House Committee on Financial Service’s Task Force on Monetary Policy, Treasury Market Resilience, and Economic Prosperity. 11

While options 4 and 5 may ease banks’ balance sheet constraints to some degree during market stresses, they are unlikely to prevent the eSLR from being the unintended primary binding capital constraint for U.S. GSIBs as they are predicated on maintaining the current leverage capital level (thus the current bindingness of leverage ratios). By contrast, adopting option 3—exempting Treasuries from all leverage ratios—would substantially ease the U.S. GSIBs’ balance sheet capacity constraints, as we have demonstrated in a previous blog. 12

The U.S. capital rules calculate the GSIB surcharge based on a systemic risk score: higher scores mean higher surcharges. This score is derived from two methods—Method 1, which follows the Basel Committee’s methodology, and Method 2, applicable only to U.S. GSIBs. Indicators include size, interconnectedness, cross-jurisdictional activity, complexity, substitutability (Method 1), and reliance on short-term funding (Method 2). Method 2 always produces a surcharge equal to or greater than Method 1, so the applicable surcharges for U.S. GSIBs are determined using Method 2.

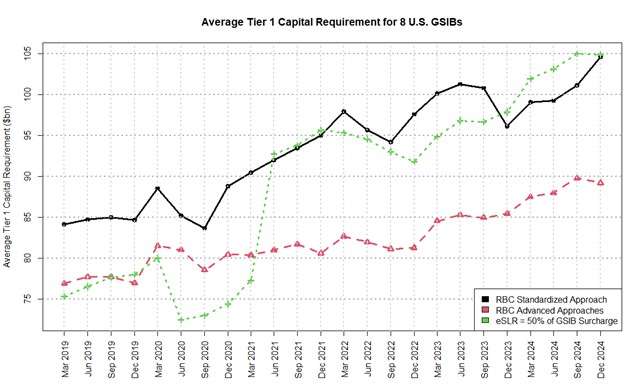

Figure 3 illustrates the impact of setting the leverage buffer at 50% of the GSIB surcharge, as proposed by the Federal Reserve Board in 2018. This measure reduces the likelihood of the eSLR (green dotted line) being the binding capital constraint for U.S. GSIBs relative to the risk-based capital requirements calculated using the standardized approach (black solid line). However, it remained binding over half of the time in June 2021 and December 2024. In addition, the leverage capital requirements would be consistently higher than the risk-based capital requirements under the advanced approaches (red dashed line).

Figure 3. The average dollar amount of risk-based Tier 1 capital requirements of 8 U.S. GSIBs calculated using both the standardized approach (black solid line) and the advanced approaches (red dashed line), and leverage capital requirements calculated using the eSLR with the leverage buffer equal to 50% of applicable GSIB surcharge (green dotted line).

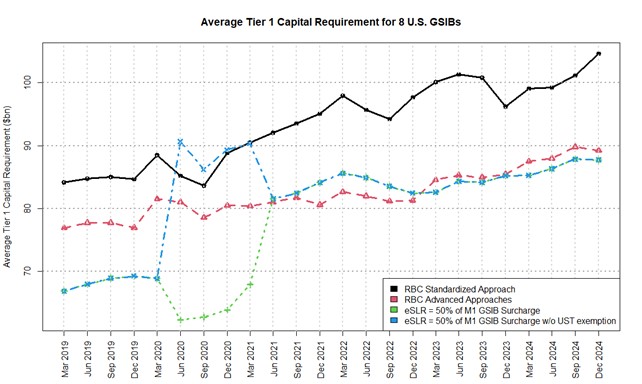

Figure 4 demonstrates the impact of setting the leverage buffer at 50% of the Method 1 GSIB surcharge. Additionally, two scenarios are evaluated: (1) considering the temporary exemption of Treasury securities and central bank reserves from SLR calculation, and (2) accounting for the Treasury securities held for trading not being temporarily exempted from the supplementary leverage ratio calculation, as detailed in the separate publication.

This measure further decreases the probability that the enhanced supplementary leverage ratio (green dotted line) will be the binding capital constraint for U.S. GSIBs compared to the risk-based capital requirements determined using the standardized approach (black solid line). However, the blue dashed line indicates that if the Treasury securities held for trading were not temporarily exempted, it would likely not alleviate balance sheet constraints during market stress events such as the COVID-19 “dash for cash.” 13 Moreover, leverage capital requirements would remain binding approximately half of the time between June 2021 and December 2024 relative to the risk-based capital requirements under the advanced approaches (red dashed line).

Figure 4. The average dollar amount of risk-based Tier 1 capital requirements of 8 U.S. GSIBs calculated using both the standardized approach (black solid line) and the advanced approaches (red dashed line), and leverage capital requirements calculated using the enhanced supplementary leverage ratio with the leverage buffer equal to 50% of the Method 1 GSIB surcharge, and with the effect of the temporary exemption of Treasury securities and central bank reserves (green dotted line) and without the effect of the Treasury securities held for trading being temporarily exempted (blue dashed line).

Conclusion

U.S. GSIBs are vital for the liquidity and stability of the U.S. Treasury markets. Because of the non-risk-sensitive nature, binding leverage ratio constraints discourage these banks from allocating capital to low-risk activities like holding Treasury securities and market-making. Therefore, reforming leverage ratios is critically necessary for these banks to support the anticipated increase in Treasury issuance over the next decade. Among the five potential options that the Federal Reserve Board could consider adopting, our analysis suggests that permanently excluding Treasury securities and central bank reserves from leverage ratios is the most effective solution, as demonstrated by the impact of the temporary exemption granted during the COVID-19 pandemic.

Author

Dr. Guowei Zhang is Managing Director and Head of Capital Policy for SIFMA

Footnotes

- https://www.bis.org/bcbs/publ/d424.htm

- https://www.govinfo.gov/content/pkg/FR-2014-09-26/pdf/2014-22083.pdf

- https://www.federalregister.gov/documents/2018/04/19/2018-08066/regulatory-capital-rules-regulatory-capital-enhanced-supplementary-leverage-ratio-standards-for-us

- https://www.sifma.org/resources/news/blog/understanding-the-current-regulatory-capital-requirements-applicable-to-us-banks/

- Data was collected from FR Y9-C and FFIEC101 reports by the 8 U.S. GSIBs.

- https://www.federalregister.gov/documents/2020/04/14/2020-07345/temporary-exclusion-of-us-treasury-securities-and-deposits-at-federal-reserve-banks-from-the

- https://www.federalregister.gov/documents/2020/01/27/2019-28293/regulatory-capital-rule-revisions-to-the-supplementary-leverage-ratio-to-exclude-certain-central

- https://www.bankingsupervision.europa.eu/activities/srep/2024/html/ssm.srep202412_aggregatedresults2024.en.html

- https://group30.org/images/uploads/publications/G30_U.S_._Treasury_Markets-_Steps_Toward_Increased_Resilience__1.pdf

- https://www.cbo.gov/publication/61172#_idTextAnchor038

- https://docs.house.gov/meetings/BA/BA00/20250408/118116/HHRG-119-BA00-Wstate-LiangN-20250408.pdf

- https://www.sifma.org/resources/news/blog/enhance-market-resilience-by-exempting-treasuries-from-leverage-ratios/

- We perform econometric analyses (using panel regression with fixed effects) to quantify the effects of the Treasury securities held for trading on banks’ supplementary leverage ratios, utilizing FR Y-9C data from the 8 U.S. SIBs for the period spanning March 2018 to December 2024.