Four Top Takeaways from SIFMA’s 2025 State of the Industry Briefing

- SIFMA Editors

At SIFMA’s State of the Industry Briefing, Ken Bentsen and Ron Kruszewski outlined the key advocacy priorities and market issues shaping the year ahead. Here are the top takeaways.

Top Takeaways

1. Market Performance: A Strong 2025 Across Asset Classes

- U.S. markets delivered strong results despite inflation, tariffs, and geopolitical risk. “We have the deepest, most liquid markets in the world,” said Kruszewski.

- The S&P 500 returned 20% YTD; equity ADV hit a record 17.7B shares (+51% YoY).

- YTD IPO issuance reached $36.1B (+20% YoY); SPAC activity almost tripled to $25.0B.

- Long-term Treasury issuance reached $4T YTD (+3% YoY) with ADV above $1T; corporate, muni, MBS, and ABS issuance also increased.

- SIFMA’s Economist Roundtable projects 2.1% GDP growth in 2026, moderating inflation, and further Fed cuts.

- Investor sentiment remains strong, with elevated but manageable volatility.

2. Regulatory & Policy Priorities to Define 2026

- Treasury Clearing: Updated implementation white paper coming soon; transition ahead of 2026–2027 compliance dates remains a top focus. “We are spending a tremendous amount of time on this,” said Bentsen.

- Capital & Leverage Framework: SIFMA supports restoring eSLR as a true backstop and improving the Tier 1 leverage ratio; the Basel III Endgame and GSIB surcharge re-proposals are expected soon. “We’re cautiously optimistic that we’ll get a more workable proposal,” said Bentsen.

- Private Markets Access & Investor Protections: We’ve seen tremendous growth in private markets, as companies stay private longer. SIFMA is working with regulators, retirement plan sponsors, and the industry to expand access responsibly, with rigorous valuation, reporting, and liquidity standards. “What’s the most practical, prudent way for everyday investors to have exposure to these markets?” asked Bentsen.

- Digital Assets, Tokenization & Market Structure: The $19B crypto flash crash on Oct. 10 underscored the need for robust investor protections. Key priorities include tokenization under existing frameworks, stablecoin rules (GENIUS Act), CAT reform, e-delivery, and equity market structure updates. “What we need to do is make these young, innovative companies available to the general public so that the rising tide of American economic activity isn’t just in the private markets – it gets back to the public markets,” said Kruszeski.

3. Investor Trust and Satisfaction High, Generational Shift on Horizon

- 8 in 10 investors are satisfied with the industry; 7 in 10 say firms act in their best interests.

- A widening generational divide: Boomers emphasize performance; Gen Z expects immediacy, transparency, and control.

- Technology has expanded access but blurred the line between investing and gambling. “Access without understanding is not empowerment,” said Kruszewski.

- With $100+ trillion set to transfer to younger generations, firms will need to balance digital convenience with education, guidance, and long-term safeguards.

4. The Market Outlook for 2026

- Equity markets expected to remain resilient, supported by earnings strength and active trading.

- Capital formation and M&A are likely to improve as financing conditions ease.

- Outlook: moderate growth, softer inflation, and gradual Fed rate reductions.

- “The market has been remarkably resilient, yet we cannot lose sight of basic fundamentals,” said Kruszewski, noting a PE near 25x and a 10-year yield above 4%. “Markets are rich in terms of valuation.”

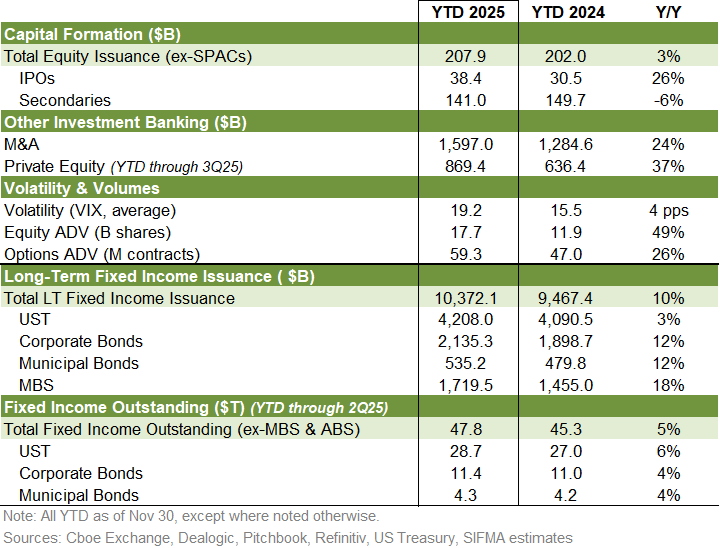

Featured Charts & Data

Transcript

Cheryl Crispen:

Good morning and welcome. Thank you for joining us today for SIFMA’s 2025 State of the Industry Briefing. I’m Cheryl Crispin, executive Vice President at SC fma, and I’m here today with Ken Benson, president and CEO of SIFMA and Ron Rusky, chairman of the board and Chief Executive Officer of Stifel, and importantly SC SIFMAs 2026 chair. We are pleased to have both members of the media and SIFMA member firms participating in today’s briefing. Ken and Ron will provide approximately 30 minutes of remarks and then we will open up the session for q and a. All participants will be muted throughout the presentation, but we would like to make this as interactive as possible, so please submit questions for Ken and Ron through the q and a box on your screen and I’ll moderate the session discussion after Ken and Ron make their remarks. Now it is my pleasure to turn it over to Ken for some highlights. Ken,

Ken Bentsen:

Thank you Cheryl and thank you Ron. Congratulations on becoming SIFMA chair for this year and thank all of you all for joining us As we have this briefing, we’re pleased to share our 2025 recap and our 2026 outlook with you. So I’d like to start with some 2025 market data as prepared by sys research group. So in the equity markets so far through 2025, we’ve seen a very strong year despite a few pullbacks amid worries over inflation, tariffs impact and geopolitical concerns. The major indices posted solid gains through November 30th, driven largely by strong corporate earnings in hopes for easing of monetary policy. S&P500 returned an impressive 16% year to date following a 23% increase for all of 2024.

As equity volumes grew significantly as well. Equity average daily trading volume was a record 17.7 billion shares through November 30th of plus 49% year over year equity volumes kept rising and hitting new highs as the ADV broke above 20 billion for the first time this October and average above 18 million in six out of the 11 months this year. As for volatility, the VIX average 19.24% through November 30 versus an average of 15.55% for all of 2024. And this elevated level occurred due to pockets of uncertainty related to not just FOMC meetings, but also heightened geopolitical tensions, tensions, tariff announcements and inflation expectations. In capital formation IPO deal value year to date through November 30th, 2025 was 38.4 billion, up 26% from the same 11 months in 2024 and moving closer in line with annual averages of 48.8 billion. Going back to 1990, the market found renewed momentum with broadening base of sectors tapping the public market so far this year, despite this uptick volumes remain well off recent peak years such as 2020 and 2021 where IPO deals totaled 85 billion and 150 billion.

Respect the activity from SPACs also increased pricing 25 billion in deals through November 30, an increase of 196% versus the same period in 2024. In the fixed income markets. We saw a treasury issuance continuing its upward trajectory in 2025, growing 3% year over year to $4.2 trillion through November 30 with treasury ADV totaling over 1 trillion through November 30 at a 16% year over year increase. In fact, ADV exceeded 1 trillion in eight of 11 months in 2025 for the full year of 2024, ADV was above 1 trillion for only one month. The corporate bond market corporate bond issuance was up 12% year over year through November 30 with investment grade up 10% in high yield up 14%. This came after already elevated issuance in 2024. Issuance already is already over 2.2 trillion. I should say year to date, A level not reached since 2021 when the 10 year yields were an average 288 basis points.

Lower corporate bond ADV increased by 12% year over year through November 30. ADV has averaged almost 60 billion so far in 2025 with four out of 11 months reporting ADV over 60 billion. Looking at other asset classes, municipal bond issuance was up 12% year over year through November 30 with trading volume averaging 15.2 billion, up 16% year over year. MBS issuance was up 18% and a BS issuance was up 21% year over year. SIFMA also last month released our semi-annual SIFMA Economist Roundtable survey results. This semi-annual survey compiles median economic forecast of SIFMA member firms. We analyzed the roundtables economists expectations for GDP, unemployment, inflation, interest rates and other metrics. Two key takeaways from the most recent survey are half the respondents are optimistic about the outlook for the US economy in 2026 versus being neutral or negative, assigning the probability of a contraction in GDP in any quarter of 2026 at just 15 to 30%.

Overall GDP growth is expected to decrease to 2% for all of 2025 and then slightly pick up to 2.1% in 2026 equivalent figures for Q4 over Q4 or 1.8% in 2025 and 2.2% in 2026 while four PC inflation is projected to decline modestly from 2024 levels to 2.9% in 2025, fourth quarter, 25 over 24, and received a 2.5% in 2026, fourth quarter, 26 over 25. Federal reserve is expected to cut rates by 25 basis points in December and another 50 to 75 basis points by the end of 2026. All forecast figures and more are available on the research section of our website at sifma.org.

Looking at some of our top priorities for the year ahead, SIFMA and MY are preparing to publish an updated white paper on treasury clearing, which is focused on dunaway clearing requirements. This update, this is an update to our November, 2024 white paper and is part of our broader efforts on treasury clearing, including the development of standard clearing documentation implementation guides and the release of a survey last month, which assessed firms readiness for transition for the transition and highlighted areas where there still needs to be more clarity. We continue to work with the industry on the transition to this new rule. The SLR proposal was finalized at the end of last month by prudential regulators and we strongly support restoring the ESLR to its proper role as a backstop for risk-based capital requirements and mitigating limitations on the ability of banking organizations to intermediate US treasury markets.

This is particularly pressing given the impending industry move to mandatory clearing for US treasuries and we commend the agencies for the focus on the issue and continue to encourage them to consider revisions to the tier one leverage ratio requirements and future rulemaking as part of the broader review of the US regulatory capital and leverage framework and the negative effects of the tier one leverage ratio on US treasury market intermediation. The Basel III endgame proposal and GSIB surcharge re proposal are expected to be released in the coming months. And SIFMA has long argued that any policy changes must recognize the role of our capital markets and the deepest, most liquid and efficient as a core component of the broader US economy. The simple will work towards ensuring that the re proposal should make substantial improvements to market risk proposals and should be considered with the existing stress testing requirements.

We look forward to reviewing the re proposal in detail. Robust investor protections are the foundation of US securities markets, ensuring market integrity and investor competence, digital asset markets, and the related technology brings both promise and efficiency and risk, particularly as it relates to tokenized securities and policymakers are right to be developing laws and rules to ensure fair and efficient markets and robust investor protection. The record setting crypto flash crash on October 10th, 2025, which wiped out nearly 19 billion in digital asset value in a single day underscores that market’s vulnerability to both external and internal shocks and the critical importance of ensuring that traditional investor protections are applied to such markets while modernization and tailoring of existing rules may be required to accommodate new technologies, investor protection and market integrity must remain central across all asset classes. Tokenization of traditional assets such as equities or bonds is a current key focus of ci.

We strongly believe that existing investor protections and market structure rules for securities must be extended to tokenized assets and related activities that are by definition securities, including the current broker, dealer exchange and custody frameworks under federal securities laws. Those market participants who seek exemptions from such rules when engaging in securities activities should have the burden of proof to explain why such rules need not applied on stablecoin. With the Genius Act now enacted, a prudential rulemaking process is underway to put finer details on key components of the act. SIFMA is working closely with our members to identify and advance key priorities related to payment stable coins throughout implementation throughout the implementation process or over. SIF continues to advocate for market structure legislation that creates comparable regulatory regime for digital assets, allowing member firms to conduct business efficiently. We are actively engaged on the issue of equity market structure as we have been for many years, particularly with respect to market data.

Our members have been weighing in on the commission’s recent review of n ms such as the trade through rule and note that any changes would result in the need for any changes would result in the need for broader changes in the overall NMS framework. We will be keenly interested in what the commission may propose SIP A is also coordinating industry work on the move of US equity markets towards a 24/7 or a 23/5 trading operation in our view, 23/5 that would operate from 8:00 PM Eastern time, Sunday through 8:00 PM Eastern Time Friday with a one hour delay exchange C. The DC previously announced that it will transition to a 23/5 clearing model by QQ 2 20 26 and several stock exchanges have received SEC approval 24 x and CE or have announced plans ASDA and SIBO for extending trading hours. Overnight exchange approvals are dependent upon the SIP being up and running and the SIP has announced plans to do so but it’s not yet filed an amendment following the SIP plan amendment.

The SIP will have to expand and update its systems to accommodate 23/5 trading. As such, the exchanges are targeting implementation by q1. SIFMA will be holding a round table with the SEC exchanges and other stakeholders on January 28th, 2026 to discuss open questions on the topic of extended trading and much work remains as SIFMA stands ready to support our members through the ongoing transition. We were also anticipating SEC action on the consolidated audit trail and were encouraged when the SEC announced its review of the cat. The cat began with a good idea giving regulators a clear review of market activity, but over time the scope expanded and its cost balloon. Today it collects too much personal data at enormous expense with governance that hasn’t kept pace with technology or privacy expectations. Our central concern is the collection of personally identifiable information oversight should never come at the expense of investor trust or market efficiency.

We believe the SEC must find the balance between effective market surveillance and the safeguarding of investors’ privacy and data and to ensure regulatory activity doesn’t compromise investors’ confidence in the system. German Atkins recently made comments, in fact yesterday I’d also like to touch on quickly. We support the enhancements to the IPO on-ramp and have shared our recommendations on this with the SEC. We also have supported focus on materiality and disclosure most recently in the previous climate disclosure rule, which has been stayed. So to have consistent, so to have consistent views on disclosure, we appreciate the focus on the ways in which disclosure, shareholdeSLR proposal reforms and other litigation reforms go together, and we look forward to the updates on the SEC’s progress on its plans here.

Another key area of focus is retail investor access to private markets. We want to explore ways for individual investors to have exposure to such markets, but they must be done pragmatically. Strong valuation practices, transparent reporting and liquidity management. Private assets can play a role in long-term portfolios, but they’re not for every investor or every plan. SA is engaging with regulators and plan sponsors to make possible make this possible. Holding valuation round tables, helping the Department of Labor and the SEC think through fiduciary standards and promoting policies that expand opportunity while maintaining discipline. Likewise, investor communications and how they are delivered is an area of ripe for review. The SEC’s delivery rules haven’t been updated in a quarter of a century. They were written for a world of envelopes and postage meters and not SIFMArtphones or secure apps. Investors today expect digital access to every part of their financial life.

SIFMA has proposed as simple as modernization, make electronic delivery the default, remove redundant consent requirements and keep investor choice. Front and center paper will always remain an option, but by request, not by default. Updating these rules will reduce costs, enhance security, and improve the investor experience. Lastly, on the investor topics, I would reiterate our support for vendor arbitration. However, it provides an efficient, fair, and investor friendly alternative to the courts. It remains subject to multiple layers of oversight and transparency and continual improvement. Preserving the enforceability of arbitration agreements is essential to maintaining timely, affordable, and equitable dispute resolution for millions of investors and the firms that serve them. At the same time, we strongly encourage FINRA to make significant reforms to ensure efficient operations and predictable and fair outcomes. These include permitting agreements to adjudicate certain narrow categories of claims in alternative forms, permitting agreements to preclude or limit punitive damage awards were permitted by applicable law, improve fairness of adjudicating form, UFI defamation claims, and amending certain procedural rules governing arbitrations and enhancing requirements to improve the arbitrator quality and accountability. With that, I want to turn it over to our chair for 2026. Stifel Chairman and CEO Ron Kowski. Ron.

Ron Kruszewski:

Well here Ken, first of all, you need some water? Oh, a lot of numbers. I won the prop. You’d say 10%.

A lot of numbers. So good morning. That was a great presentation. I want to thank all of you for joining us today. Before I begin, I want to make one thing clear. Clan always wants me to say that the views I express are my own and do not necessarily reflect both of SIFMA. And although for the record, they did approve my remarks this morning, I’d like to begin, Ken, we did a recent survey of the voice of investor satisfaction trust and advocacy. It was a survey conducted independently by KPMG and we asked more than 2000 investors about their confidence, trust, and satisfaction with the firms and advisors who serve them. And I thought, I know you thought, Ken, that the results were encouraging. Eight and 10 investors say they’re satisfied with the industry and nearly seven in 10 believe that we act in their best interests.

Confidence is high, but when you look closer, you see a clear generational divide. Younger investors like the, I mean the first digital native generation are engaging with markets in a completely different way. Nearly three quarters of baby boomers say performance matters most, but only a third of Gen Z says the same. Think about that. Only a third of Gen Z think that performance matters, and I think we need to dig into that a little bit. They want immediacy, transparency, and control. They like the speed and the access that many prefer in many of those today prefer to invest on their own. Now, none of this is bad. It’s the world that we’ve built. Technology has opened the doors of finance wider than ever before, but has also brought the impulses of gambling into the world of investing. The art of investing frankly, is beginning to share space with a dopamine rush of speculation and what started with zero day options and perfs have now expanded into prediction markets and prop debts.

I believe a new form of gambling dressed up as financial innovation. It’s an AC industry operating through regulatory loopholes and it blurs, in my opinion, the line between investing and entertainment in ways that really should concern all of us. From the investment point of view, investment really was never meant to be entertainment. Access without understanding is not empowerment, it’s exposure. And when markets start to feel like games, the purpose of investing, which is to create lasting financial security, I think it’s lost in the noise. Recently I wrote an op-ed in Barron’s making exactly this point. We need to remind the next generation and all investors, frankly, the next generation is set to invest, inherit more than $100 trillion in the next two decades. And I think as an industry is responsible, we educate them that investing and gambling are not the same thing. One builds the other burns and I tell them they need to understand.

Young investors, I’ll get asked often, what words can you tell me quickly that I need to understand? I say, you need to understand the power of compounding versus the fun of consumption. Investing is compounding, gambling is consumption, but I admit watching money compound is not as exciting as making that parlay bet. So as we close out the year, I’d like to offer some market perspective where we stand today and what we see as we head into 2026. As for the economy, I see robust m and a and equity markets activity as we head into 2026. The market has been remarkably resilient, yet we cannot lose sight of basic fundamentals. We’re operating with a price earnings multiple around 25 times and a 10 year yield above 4% by any historical measure. Markets are rich in terms of valuation. I’m somewhat old school and I look at a simple measure.

I look at the nominal equity risk premium today, it’s roughly zero, which suggests that equity investors may not be properly compensated for the risks that they’re taking on Federal Reserve policy. While it seems likely the Fed will cut rates, again, I’m in the camp that we should be more measured. Prices are up roughly 25% since 2020. Consumer prices is what I’m talking about. And wages have not kept pace. That gap matters. And for that reason I see the resurgence of inflation as the greater risk going forward. What we’ve presented today is not an exhaustive list, although it was quite long. I’m not sure I want to stay for that job. Yeah, there’s a lot to do, but it’s not an exhaustive list of what S will be focused on in the coming year. We have a great deal more to talk about, so let’s open up the discussion for any questions out in cyberspace.

Cheryl Crispen:

Great, thank you Ron. And thank you Ken. Again, if you would like to ask a question, I have a couple that have come in already. Please do go down to your q and A button on your zoom screen and submit your question. The first question here, SIFMA recently submitted a letter to the SEC emphasizing that tokenized assets must preserve full legal and beneficial ownership with the SEC’s investor advisory committee hosting a meeting panel tomorrow, it says here, what does SIFA hope to come out of that discussion?

Ken Bentsen:

So it’s a good question. So our focus with the SEC specifically has been largely with respect to tokenized securities. We do comment on broader digital assets, but in particular assets that are either true tokenized securities or reference securities. And there what we’ve actually submitted, I think now five different letters to the SEC, the crypto task force, we submitted a letter to Chairman Atkins and the commissioners last week reiterating many points, and these are when something is deemed as security. And the SEC has been pretty clear on this of saying when something is a security in whatever form it may be, it is a security. We’re saying the rules of the existing security laws should apply and if for some reason the current form of that law, there’s a problem with it applying to a digital security, what is that and how can that be resolved?

But what you can’t do is water down the rules for something that is a share of apple, whether it’s in a paper form, which no one has, or a digital form or a book entry form. And I think I would give credit to the commission to Chairman Atkins, commissioner Purse, the investor advisory council that’s meeting today, that the SEC has really dug into the issue of digital assets broadly and in particular when digital assets are securities and really digging into understand what they are, come up with a taxonomy, come up with a definition and understand what rules should apply. And because policymakers do have a responsibility here as this marketplace has developed in ensuring that there’s robust investor protection like that that we live with in the securities world, we’ll be very eager to see what the IAC comes out with. I dunno if

Ron Kruszewski:

Ron, look, I think tokenization does need to have the legal basis of what it is. The security sitting at DTC are, they’re digital. I mean I haven’t seen a paper certificate in years, but some token as token securities are really derivatives. And I think we’ll get around to that, but it’s important.

Cheryl Crispen:

Great, thank you. Another question here, I think this might be from a member, how will FMA continue to work with firms on treasury clearing changes and what are some of the hurdles to the new treasury clearing infrastructure?

Ken Bentsen:

Right, so there’ve been a number of work streams on this. So let’s remember. Cash treasuries will be subject to mandatory clearing at the end of 26 with repo at the end of midyear 27. And since that rule was initially promulgated back in 24, we’ve been working with our members buy side and sell side on a number of issues. Obviously a tremendous amount of work on creating standardized documentation for both done with and done away. The done with documentation’s been done, the done awake documentation will be done shortly. I mentioned in my remarks, we have a new white paper coming out that we’re doing with EY on implementation and issues around Dunaway. We did one last year with respect to done with and then we’ve been working and engaging primarily with the SEC, but also with the Prudential regulators on various issues that either in the final rule that were not completely clarified around things like inter affiliate transactions or mixed CUSIP transactions and likewise netting issues that potential regulators need to deal with.

And we continue to work through those. And then also noted, we recently conducted a survey with a number with BNY and PTCC and others of surveying the industry both in the US and around the globe in terms of their readiness for moving to this. And what we did see was in the US pretty good awareness of what’s coming, but still work to be done as firms prepare for this, both buy and sell. But as we went outside the US more work to be done. And so we’re engaging closely as well with our colleagues at our sister organizations in Europe and in Asia as well as with other trades. I’ve raised this with iosco, the Association of Securities Regulators around the globe, that this is something where we need an all hands on deck and I give kudos. Also, I want to give kudos to SEC Commissioner Mark Ada, who’s really taken the lead on behalf of the SEC and shepherding this through. And I know Commissioner U has been doing a lot of work, not just in the US and talking to the industry, but talking to his counterparts around the globe because obviously as we all know, it’s a global market. And lastly, I should note, we’re also very engaged with the Treasury Department, their market, and so we are spending a tremendous amount of time and effort on this.

Cheryl Crispen:

Great, thank you. Here’s another question, Ron, I think more directed to you. Ron mentioned the SIFMAs investor survey and highlighted some of the trends that are reshaping investor expectations. Ron mentioned his Baron’s op-ed about blurring the lines between investing and entertainment. Ron, and maybe then also Ken, how are some of the findings from the survey impacting SIFMAs priorities for the year ahead?

Ron Kruszewski:

For me, it shines a light on the importance of investor education and that what we talk about and investing and the compounding and the effects of sharing in the US economy, that is very important and that it’s the industry’s job to educate younger people about investing. And so that’s my biggest takeaway. There’s some things that have never changed. Young investors always start investing by themselves and they’ll evolve. That was true 20, 30 years ago. I always said it was true when I was a Gen Z or it was a long time ago, but education, I don’t know what you would add

Ken Bentsen:

To that. Yeah, no. So a hundred percent, I mean first of all in education and a shout out to our affiliated SIFMA foundation that runs a number of programs with schools touching almost a million students around the country every year in particular with the stock market game. These are kids in middle school and high school that are doing this, and that’s a great program and there are lots of programs, but that’s a program and we need to be doing more of that. I think the other thing that we picked up from the survey was between the boomers like you and me all the way to the Gen Zers and others, there are different gradations of their engagement in terms of investing and how they invest in how they work with the financial advisor. And I think there’s a lot for the industry to learn from that. And then I think the other thing that came out of that was, and I mentioned this, it may seem trivial, but it’s not, is the application. Ron talks about apps and how you even communicate with your clients at Stifel, but things like eDelivery that you have to be able to communicate with your clients across the generations in many ways in a more electronic thing. So I think things like that certainly fit within our general.

Cheryl Crispen:

Great. Next question here, and again, if you would like to ask a question, please use the q and a at the bottom of the screen. If you could please explain the benefits and detriments of allowing publicly traded companies to post reports semi-annually instead of quarterly.

Ron Kruszewski:

Well, I can start with that. I mean, the benefits would be that there’s a tremendous amount of overhead to just report the cues under the rules, the rules, and that you would take away a lot of that expense. And short term thinking is one of the other things that they say. And you would go to a six month reporting. But what I would say is that, and by the way, that could be important for new companies coming up, new companies, and I think that we are trying to make it easier to go public. But what will happen here, and I think we got to be a little more pragmatic about this, is that the market will dictate, I believe that I would still report quarterly because my investors would demand it. We have to do what our investors want, but it would not be required to follow the Q process. You can do that. So it’s a nuanced thing. There’s a lot of people that think quarterly reporting is changing behavior, for one, want to be cautious because we have the deepest most liquid markets in the world, and I don’t like fussing with that too much.

Cheryl Crispen:

Yep, fair. That’s great. Ken mentioned eDelivery as part of the investor sort of engagement and satisfaction in delivering information. Ken, can you update on what the status of eDelivery is either with regard to the SEC or any legislative activity?

Ken Bentsen:

Sure. So a couple of things. We’ve certainly engaged with the SEC on this issue. We have given them a submission that really detailing all of the different changes that would need to be made in various rules to make eDelivery a default. And just to back up on that, what we’re suggesting and what we’re proposing is where a client has an active email address with their firm, with their broker that they deal with, that that can shift to a default to eDelivery. But at any time, as many times as that client wants, they can go back to that to their broker and say, I want PayPal. So they’re not forfeiting their ability to get paper, but they’re just hastening the shift to electronic communications, which in many cases is probably more secure than getting physical mail, which can get lost or stolen. So we’ve written to the SEC after discussing this with them and said, here are all the things you would need to do to do this, and it’s well within your authority to do it. At the same time, we have been working with our members in pursuing a legislative fix. So just putting this in statute, and some may recall that in the last Congress, the house passed a bipartisan bill overwhelmingly to make eDelivery the fall, and the Senate had bipartisan legislation introduced, it didn’t get taken up. There’s been bipartisan legislation introduced in both the House and Senate this year, and that would be great to go by that route. So we’re sort of looking at a two track strategy.

Ron Kruszewski:

I just have to add, to me, it’s ridiculous that we’re sitting here today talking about modernizing treasury clearing, the blockchain, digitization of assets. Everything’s on an app. The survey says investors engage digitally, yet we still have a rule that requires paper is beyond ridiculous. I think the problem is is that we have so many rules that we have to figure out what it touches, but that’s the complexity because this is not going to T one where the industry does. Everyone in the industry already will send electronic and the clients, they can get paper because we send a PDF form, they can just hit their printer or they can call us, we’ll go out to mail it to ’em. I got to tell you again, if this one can’t get done, then none can get done because this is so simple and one of the few rules saves a lot of money and frankly is environmentally conscious people don’t want to say that. So let’s get this one done.

Cheryl Crispen:

Great. Perfect. Thank you. Here’s another one. Maybe if you could discuss general efforts to and sima’s work on encouraging the SEC to update their books and records rules.

Ken Bentsen:

So I think this is may be going to issues around communications. And this is an issue that has really brought to light with the recent enforcement actions around texting and the like. To Ron’s point, there’s a robust rule book on the whole, that rule book is very important, very good in making sure that we have market integrity, investor confidence, fair and orderly markets. But what we found is that with lack of clarity, basically the commission has been able to bring enforcement actions on things that are foot faults or maybe not even foot faults. And really there’s no, the firms need to understand they’re making when they’re really trying to make best efforts to ensure they’re meeting their books and records requirements that they’re not sort of getting caught up with almost like a speed trap type situation. And so this is something that created a lot of frustration with our members, affected virtually every broker dealer started to move towards the asset management side and then stopped. And so we have been talking to the commission about show us what success is here because the firms really do want success. I mean, they want to be able to comply with the rules as they are, but to be sort of cherry picked with almost supposed footballs or whatever just doesn’t seem to make sense. How can we all get together and say, what does success look like here?

Ron Kruszewski:

Yeah, I would say that also all the firms I talked to want to use the enhancements that AI can do for productivity and they simply want to do it. However, most of those are organizational tools. They can summarize notes, they can do a number of things that make it very efficient. But in our business, many of the notes we take are just musings of trying to get to a conclusion they’re not final. And if we’re required somehow to take things that were never put to any use and then supervise it and record it, it is really difficult. So the rule book as it relates to electronic communications just needs to be updated to the modern day that we live in. It’s difficult,

Ken Bentsen:

But we need to do it. And it is a key priority for us this year.

Ron Kruszewski:

And I think the SEC recognizes, I agree.

Cheryl Crispen:

Here’s another one. Do either of you want to comment on Chairman Atkins remarks with regard to small company IPOs that he made yesterday?

Ken Bentsen:

Go

Ron Kruszewski:

Ahead for a

Ken Bentsen:

Second. Yeah, so we were encouraged by those remarks. We’ve been very supportive of previous efforts like Congress and previous administrations through things like jobs Act 1.0 2.0, the development of an on-ramp for emerging growth companies. I think some of the stuff Chairman Atkins talked about yesterday was sort of taking that concept, the emerging growth of companies and updating it to where we are today. It goes into things like reporting and giving a longer runway for those smaller companies to go public. So we were very encouraged by the comments and we were eager to see what the commission is going to propose on those.

Ron Kruszewski:

And it’s needed. I was listening to your remarks. You were commenting about the average IPO volume going back to 1990, which we haven’t gotten to, but there’s been inflation since 1990 that really tells you how difficult this market’s coming. When I talk to boards and talk to them about whether or not they want to go a private equity route or go a public route, the brand for public is very expensive, very complex, highly litigious. It can be. And so I was very encouraged by Chairman Atkins remarks because what we need to do is make these young, innovative companies available to the general public so that the rising tide of American economic activity isn’t just in the private markets. It gets back to the public markets. And I am excited about that.

Cheryl Crispen:

Great. And this may be our last question that I have here in the queue, unless anybody who’s on the line would like to ask a question, please do. So can, you mentioned private markets, private credit and the work that SIFMA is doing. Can you go into a little bit more detail on why that is a priority and also how will that impact investors and what are some thoughts for member firms in that space?

Ken Bentsen:

And then Ron can fill in here in his views. So a few things on this. So we undertook last year or the beginning of this year I should say, and we’ll continue to work on next year, a couple of work streams in the private market space. One is looking, as I pointed out as policymakers in particular Department of Labor, which has jurisdiction over retirement accounts, things like 401ks and the like, and the SEC, which has jurisdiction obviously over investor accounts, what we might call non-qualified non-retirement investor accounts, although they do have jurisdiction over IRAs as well, that’s another story. But they are thinking about how to allow or make it easier for individual investors to have exposure to private market assets. And part of the reason for that is because as Ron pointed out, we’ve had a tremendous growth in private markets. Companies staying private, staying private for longer as IPOs are down, what Akron said yesterday, 40%, but way down from where they were 2000, maybe that number was too high, but they’ve gone down well, low, we had a little uptick in 2021 and then kind of flattened out.

And so policymakers are thinking, how can we make it that where today you have institutional investors, high net worth accredited investors have access to these markets, but everyday investors don’t. The most practical prudent way for such investors to have exposure to these markets. At the same time, we’re also seeing development. We’re seeing large asset management companies, traditional forti act companies who are looking at putting together, creating products with private market assets. So there’s a whole ecosystem taking a look at this. And so we’re working with our members on both the buying the sell side as well as what regulators may do on how we might help facilitate this. Now, there are a lot of issues around this, and we’ve talked about it at our board. There are issues around valuation, transparency, liquidity in those markets. We’ve done recently did a round table on how the private market industry does valuation, how that works.

We’re doing another one on transparency and liquidity at another round table in January. And so I think there’ll be more work done on that. I think the policy makers are very eager to see how that would apply. But the other area where we’re doing work is more on the operational side and looking at the post-trade process around private markets, it is different than the public markets and how post-trade works there. And so our operations group working with members is doing that. So a lot of work to come on. This is sort of, there’s a desire among policy makers to move in this direction. The market seems to be moving in this direction, but there’s still a lot of work to be done. And it’s both as I see it from a SIFMA perspective. It’s both on the manufacturer side but also on the distribution side. Right. There are two parts to this.

Ron Kruszewski:

Yeah, I thing I would add, I’d probably just take a higher level Ken, just say that the industry, the markets have evolved after the financial crisis, we put a lot of rules on the banking system and you can measure risk in the banking systems 10 ways a Sunday. Alright, SLR leverage ratios, everything. But what’s happened is that we’ve moved the risk out of the banking system. The banks are as healthy as they’ve ever been, but the risk hasn’t disappeared. What it’s done is it’s moved into the private markets and I’m just not sure we really understand the amount of leverage, what happens in the liquidity. Everyone relies on the fact that it’s not the banks, it’s the investors now and there’s a bigger pool of capital. But I think we need to be cognizant and trying to understand what’s moved out of the regulated markets and what is more unregulated in terms of leverage and all the things we’re talking about. But that’s future, not anything that big of a concern, it’s just markets have changed.

Cheryl Crispen:

We did get one additional question that came in. If we can talk a little bit more about SIFMAs priorities with regard to Basel III end game re proposal.

Ken Bentsen:

So this is something we’ve been working on for more than a decade, and as policymakers, I think there was a Basel III endgame proposal, which came out about two years ago. It had a lot of problems with it. And in particular where our concerns are at SIFMA is around the impact on the trading book and our focus is on bank dealer activities. And the proposal that came out was very negative towards and very punitive, I should say, towards trading book activities of large dealer banks operating in the United States. And this is compounded by the stress test regime, which ends up resulting almost in a double count. And so we’ve done a lot of analysis over the last couple of years and weighing in with the regulators and showing across different asset classes where you come up with punitive risk weights that almost do make it in some cases economically inefficient to be engaged in certain capital markets activities.

And the problem with that is that the US is heavily dependent on capital market activities to drive the economy. And that’s a good thing. You look around the globe, you have businesses around the globe, you look around the globe and other jurisdictions, Europe, Asia are trying to drive more towards capital markets and funding the general economy. So I think policymakers are starting to understand that. Obviously we’re very encouraged by Vice Chair Bowman in the work that she’s doing at the Fed to come up with a new Basel III endgame proposal, but also importantly relooking at the stress test regime and understanding how that engages with the FRTB and the trading book portion of the Basel III endgame. And Ron mentioned the SLR, we had the ESLR. So we are finally getting to a point 10 years, 15 years after the crisis where we put in all these new rules and we’re stepping back and saying how do they interact with each other and what are the consequences of it? So we’re cautiously optimistic that we’re going to get a more workable proposal that is not punitive towards bank dealer operations, which are critical to the operations of US capital markets, which by extension are critical to the operation and funding of the US economy.

Ron Kruszewski:

Yeah, I’ll just say one thing and that is end game. You got to get to the end game. Okay. I mean, we’ve been talking about Basel III end game for a while, so let’s just get this done.

Cheryl Crispen:

Well great. Well thank you very much Ron and Ken, thank you to all of the media that joined the call. If you are a member of the media and you have any additional follow-up, please do reach out to SIFMA’s Communications Department. If you are a member of SIFMA and have any additional questions, please reach out to our membership department and we are very pleased for everybody joining. We thank you and again, thank you Ron and Ken. Thank you.